LFP Battery Recycling in Europe Gains Momentum with Hydrometallurgy, Utility-Scale Energy Storage Decommissioning, and Black Mass Recovery Driving Circular Economy Growth

NEWARK, DE / ACCESS Newswire / April 17, 2026 / According to the latest analysis by Future Market Insights, Europe's energy transition is quietly entering its next critical phase: what happens after batteries retire. As the first wave of grid-scale storage systems approaches end-of-life, the LFP Battery Recycling Solutions for Stationary Storage Market in Europe is shifting from a fragmented, compliance-driven activity into a structured, high-growth industrial ecosystem.

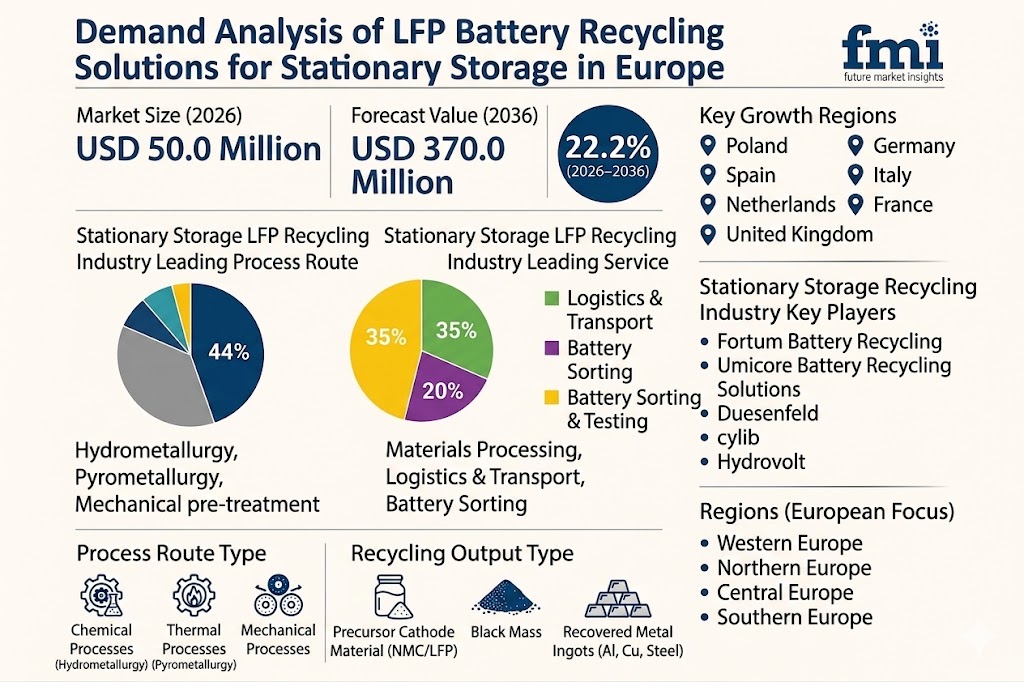

Valued at USD 50.0 million in 2026, the market is projected to surge to USD 370.0 million by 2036, registering a remarkable CAGR of 22.2%, according to Future Market Insights (FMI). This growth signals a decisive move toward formalized recycling infrastructure as utilities, regulators, and recyclers align around circular economy mandates.

Get detailed market forecasts, competitive benchmarking, and pricing trends:

https://www.futuremarketinsights.com/reports/sample/rep-gb-32694

Quick Facts & Market Snapshot

Market Size (2026): USD 50.0 Million

Forecast Value (2036): USD 370.0 Million

CAGR (2026-2036): 22.2%

Leading Process Route: Hydrometallurgy (44% share)

Dominant Source Segment: Utility-scale systems (49% share)

Top Output: Black mass (46% share)

Primary Growth Driver: Regulatory enforcement + grid-scale battery retirement

The Structural Shift: From Waste Handling to Resource Recovery

The European battery recycling landscape is no longer centered on disposal-it is rapidly evolving into a materials recovery industry. As stationary storage systems age, operators face a fundamental challenge: extracting value from lithium iron phosphate (LFP) chemistry, which lacks the high-value metals found in nickel-based batteries.

This has forced recyclers to rethink their economic model.

Rather than targeting select metals, operators are now optimizing total material recovery, monetizing lithium salts, graphite, and iron phosphate collectively. Delayed processing increases compliance risks and costs, making timely recycling not just an environmental obligation-but a financial necessity.

Process Innovation: Why Hydrometallurgy Leads

Hydrometallurgy is emerging as the dominant recycling pathway, accounting for 44% market share in 2026, due to its superior recovery efficiency for lithium-based chemistries.

Unlike mechanical shredding or pyrometallurgy, this aqueous chemical process enables:

Higher lithium recovery rates

Better purity in downstream outputs

Enhanced value realization across multiple materials

However, this advantage comes with trade-offs-high capital expenditure, reagent costs, and wastewater management requirements. Profitability hinges on achieving consistent throughput and high recovery efficiency.

Utility-Scale Dominance: Volume Drives Economics

Utility-scale battery systems are expected to command 49% of the market share, shaping the industry's growth trajectory.

The reason is simple: scale simplifies logistics.

Large, centralized battery installations:

Reduce collection complexity

Lower transportation costs per kilogram

Enable long-term recycling contracts

Early adopters-such as grid-balancing and frequency-response projects-are now entering replacement cycles, creating the first significant wave of recyclable material.

Speak to Analyst: Customize insights for your business strategy: https://www.futuremarketinsights.com/customization-available/rep-gb-32694

Black Mass: The Industry's Commercial Backbone

With 46% share, black mass remains the most traded intermediate output in the recycling chain.

This powdered material-containing lithium, graphite, and other active elements-offers:

Faster monetization cycles

Lower capital requirements (vs. full refining)

Flexibility for recyclers to scale operations

However, value realization depends heavily on quality. Impurities such as aluminum or copper can significantly reduce pricing, making advanced sorting and separation technologies a competitive differentiator.

Regional Dynamics: Uneven but Accelerating Growth

Eastern Europe: Early Processing Hub

Countries like Poland are emerging as recycling leaders, driven by proximity to battery manufacturing and early infrastructure development.

Poland CAGR: 25.8%

Southern Europe: Fragmented but Expanding

Driven by solar-plus-storage deployment, markets like Spain and Italy rely on localized preprocessing due to dispersed assets.

Spain CAGR: 24.9%

Italy CAGR: 21.5%

Western Europe: Industrial Advantage

Established industrial ecosystems give countries like Germany, the Netherlands, and the UK a head start in scaling advanced recycling systems.

Netherlands CAGR: 24.2%

UK CAGR: 23.4%

Germany CAGR: 21.9%

Regulatory Pressure: The Catalyst Behind Growth

Europe's tightening Extended Producer Responsibility (EPR) frameworks are fundamentally reshaping the market.

Battery owners can no longer delay end-of-life decisions. Compliance now requires:

Traceable recycling pathways

Certified processing facilities

Safe handling and discharge protocols

This regulatory push is steadily expanding the addressable recycling volume, even as operational bottlenecks-such as permitting delays and discharge capacity-slow actual throughput.

Emerging Opportunities: Where Value Will Be Created

The next decade will see innovation across multiple fronts:

Direct Cathode Regeneration: Reduces processing intensity while preserving material structure

Graphite Recovery: Unlocks additional revenue streams from anode materials

Mobile Pretreatment Units: Enable on-site discharge and shredding for utility-scale systems

These advancements are expected to improve margins while reducing logistical complexity.

Competitive Landscape: Technology Over Scale

The market remains technology-driven, with leading players focusing on process efficiency and material purity rather than price competition.

Key Players:

Fortum Battery Recycling

Umicore Battery Recycling Solutions

Duesenfeld

cylib

Hydrovolt

Stena Recycling

tozero

Established operators benefit from existing permits and infrastructure, while new entrants must innovate around low-impact, regulation-friendly processes to gain traction.

The Outlook: A €370 Million Circular Economy Opportunity

By 2036, LFP battery recycling for stationary storage in Europe will transition from an emerging niche into a core pillar of the energy storage value chain.

As battery deployments scale and regulatory frameworks tighten, recycling will no longer be optional-it will be embedded into project economics from day one.

The winners in this market will be those who can:

Secure long-term feedstock agreements

Achieve high recovery efficiency

Navigate Europe's complex regulatory landscape

In the broader context of the energy transition, this market represents a crucial step toward closing the loop in battery supply chains, transforming end-of-life assets into a sustainable source of raw materials.

Unlock 360° insights for strategic decision making and investment planning:

https://www.futuremarketinsights.com/checkout/32694

Related Reports:

Stationary Battery Storage Market- https://www.futuremarketinsights.com/reports/stationary-battery-storage-market

HVAC Control System Market- https://www.futuremarketinsights.com/reports/hvac-control-system-market

HVAC Market- https://www.futuremarketinsights.com/reports/hvac-market

About Future Market Insights (FMI)

Future Market Insights (FMI) is a leading provider of market intelligence and consulting services, serving clients in over 150 countries. Headquartered in Delaware, USA, with a global delivery center in India and offices in the UK and UAE, FMI delivers actionable insights to businesses across industries including automotive, technology, consumer products, manufacturing, energy, and chemicals.

An ESOMAR-certified research organization, FMI provides custom and syndicated market reports and consulting services, supporting both Fortune 1,000 companies and SMEs. Its team of 300+ experienced analysts ensures credible, data-driven insights to help clients navigate global markets and identify growth opportunities.

For Press & Corporate Inquiries

Rahul Singh

AVP - Marketing and Growth Strategy

Future Market Insights, Inc.

+91 8600020075

For Sales - sales@futuremarketinsights.com

For Media - Rahul.singh@futuremarketinsights.com

For web - https://www.futuremarketinsights.com/

SOURCE: Future Market Insights, Inc.

View the original press release on ACCESS Newswire