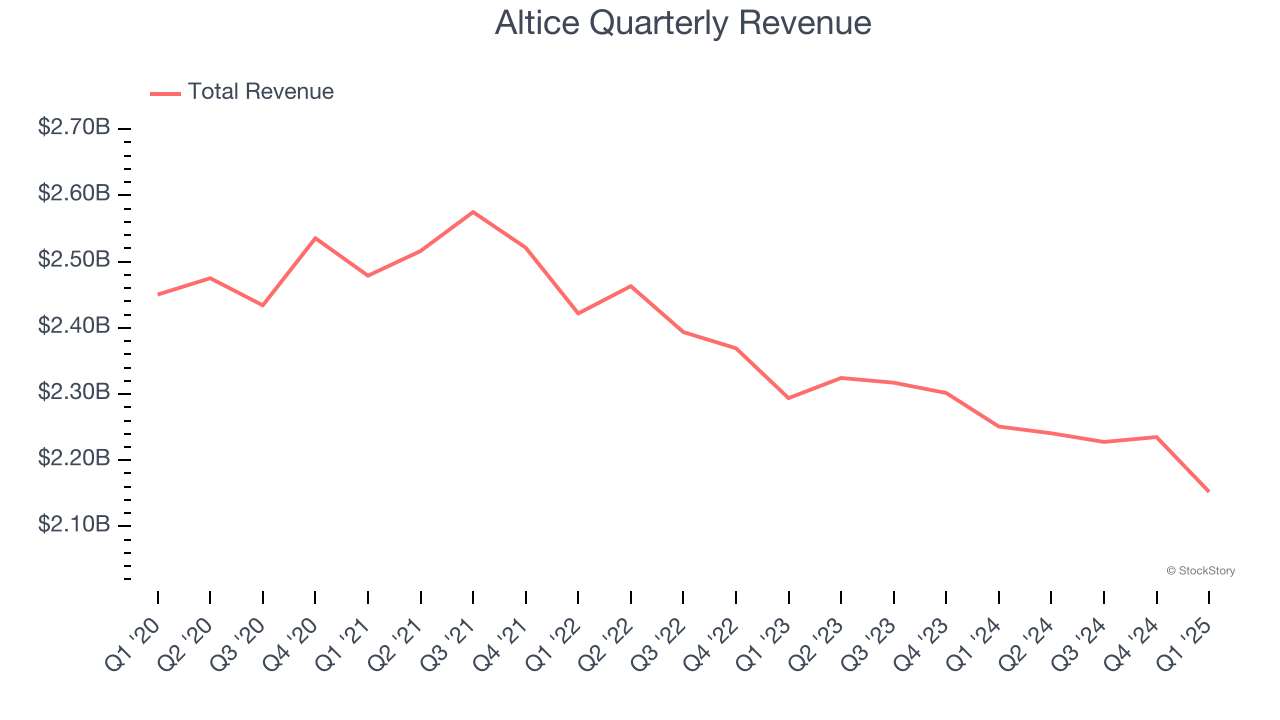

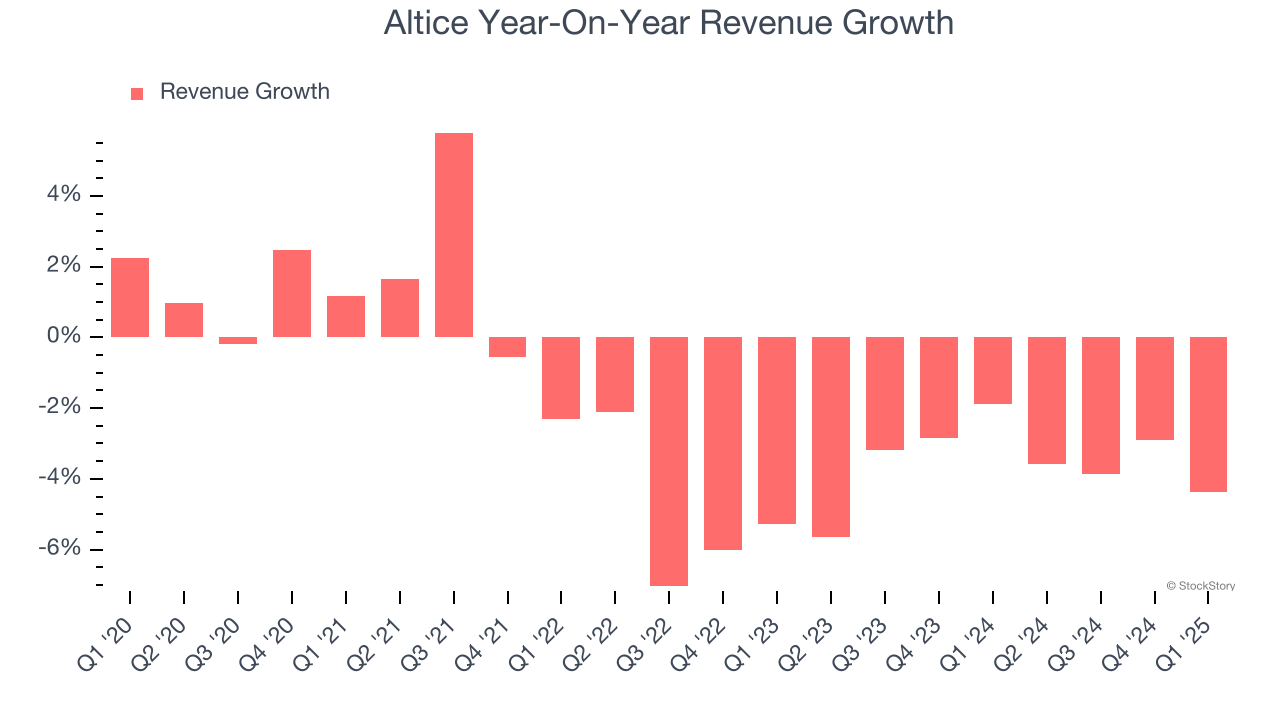

Telecommunications and cable services provider Altice USA (NYSE: ATUS) met Wall Street’s revenue expectations in Q1 CY2025, but sales fell by 4.4% year on year to $2.15 billion. Its GAAP loss of $0.16 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Altice? Find out by accessing our full research report, it’s free.

Altice (ATUS) Q1 CY2025 Highlights:

- Revenue: $2.15 billion vs analyst estimates of $2.16 billion (4.4% year-on-year decline, in line)

- EPS (GAAP): -$0.16 vs analyst estimates of -$0.08 (significant miss)

- Adjusted EBITDA: $799 million vs analyst estimates of $810.8 million (37.1% margin, 1.4% miss)

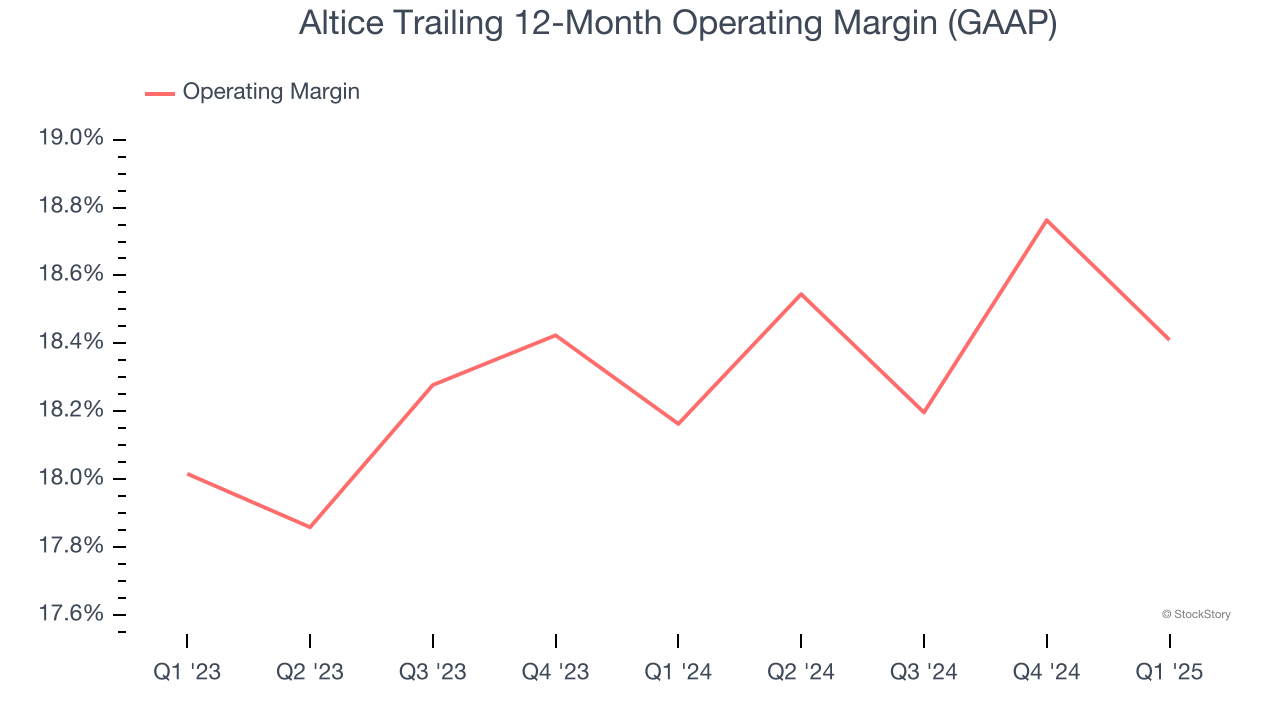

- Operating Margin: 16%, down from 17.5% in the same quarter last year

- Free Cash Flow was -$168.6 million, down from $63.57 million in the same quarter last year

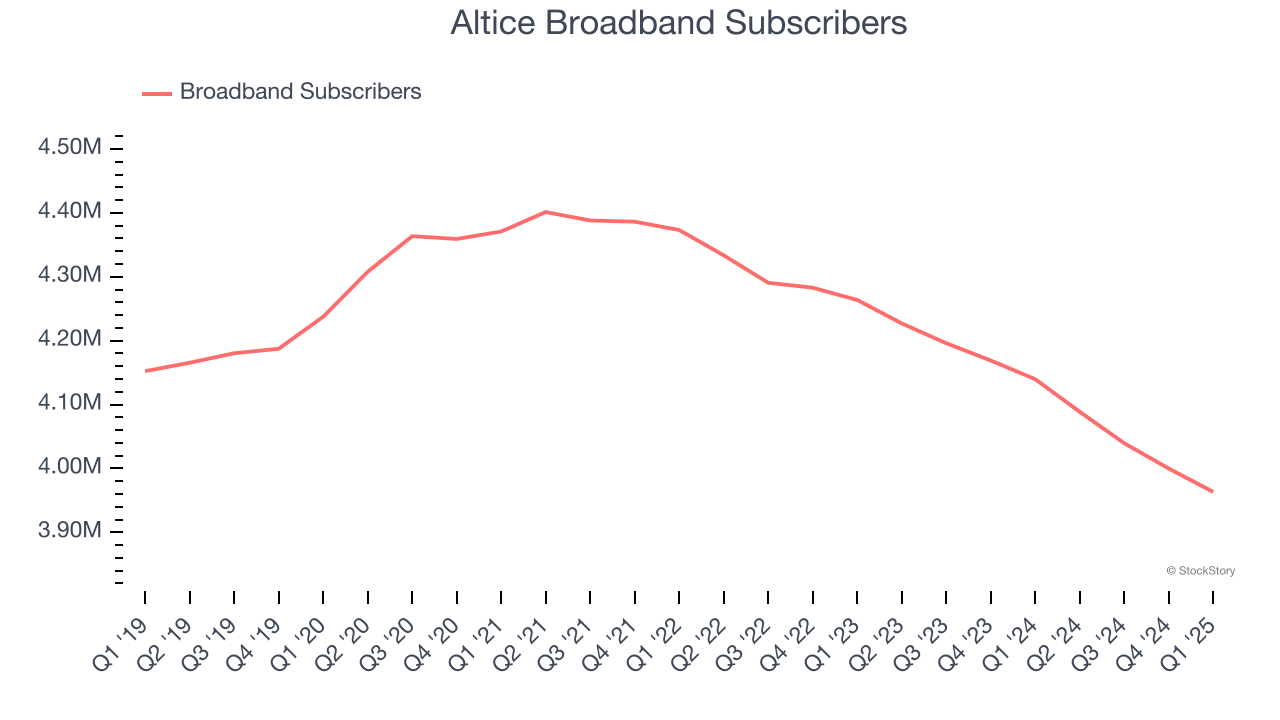

- Broadband Subscribers: 3.96 million, down 176,400 year on year

- Market Capitalization: $1.24 billion

Dennis Mathew, Altice USA Chairman and Chief Executive Officer, said: "Our first quarter results reflect steady progress against our operational and financial priorities. We achieved record customer growth in our fiber and mobile businesses and saw sequential improvement in our broadband subscriber performance, all while successfully completing two major programming negotiations with favorable outcomes and minimal disruptions to our customers. We are activating competitive strategies with enhanced go-to-market effectiveness, deepening penetration of both new and existing products, and transforming our operations to drive efficiency, leading to our lowest churn levels in three years. Based on our continued progress and momentum we expect to deliver approximately $3.4bn of Adjusted EBITDA in Full Year 2025, representing a meaningful improvement from prior year trends, as we stay focused on sustainable growth, shareholder value, and delivering best-in-class services to the communities we serve."

Company Overview

Based in Long Island City, Altice USA (NYSE: ATUS) is a telecommunications company offering cable, internet, telephone, and television services across the United States.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Altice struggled to consistently generate demand over the last five years as its sales dropped at a 2% annual rate. This was below our standards and is a sign of poor business quality.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Altice’s recent performance shows its demand remained suppressed as its revenue has declined by 3.5% annually over the last two years.

Altice also discloses its number of broadband subscribers and pay tv subscribers, which clocked in at 3.96 million and 1.79 million in the latest quarter. Over the last two years, Altice’s broadband subscribers averaged 3.2% year-on-year declines while its pay tv subscribers averaged 12.1% year-on-year declines.

This quarter, Altice reported a rather uninspiring 4.4% year-on-year revenue decline to $2.15 billion of revenue, in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to decline by 4.1% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and indicates its newer products and services will not catalyze better top-line performance yet.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Altice’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 18.3% over the last two years. This profitability was top-notch for a consumer discretionary business, showing it’s an well-run company with an efficient cost structure.

This quarter, Altice generated an operating profit margin of 16%, down 1.5 percentage points year on year. This reduction is quite minuscule and indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

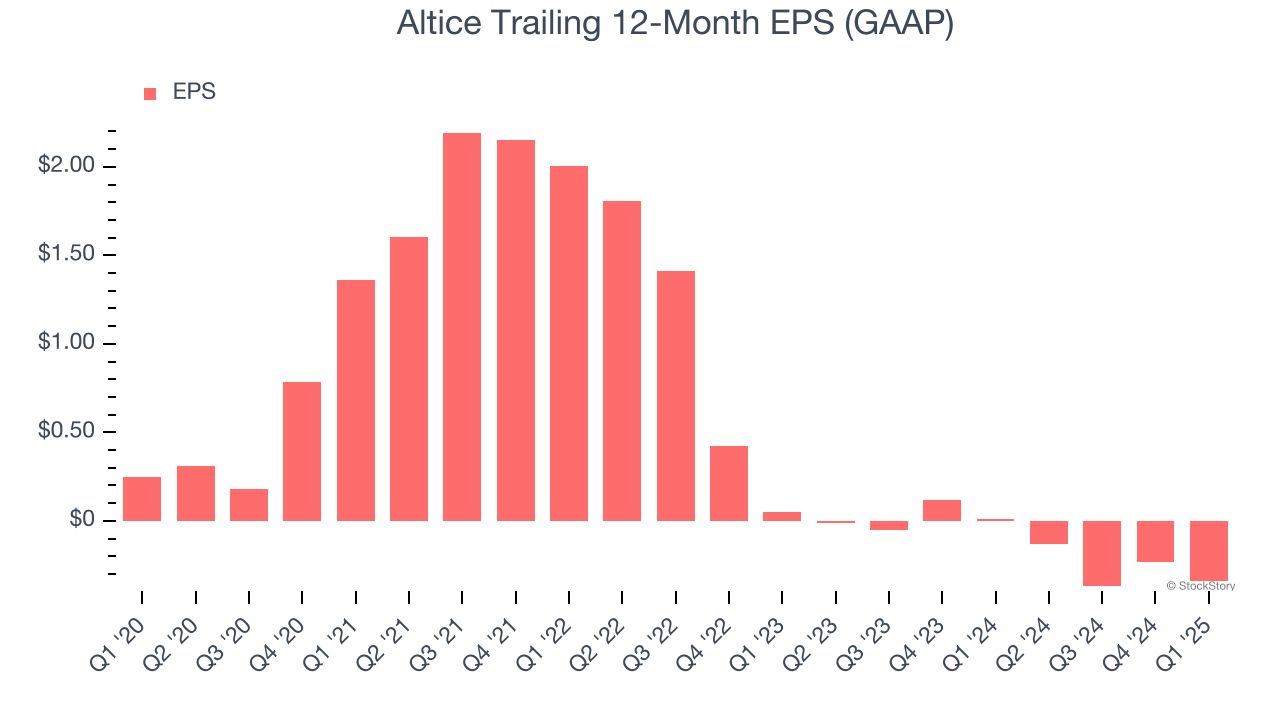

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Altice, its EPS declined by 27.4% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

In Q1, Altice reported EPS at negative $0.16, down from negative $0.05 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast Altice’s full-year EPS of negative $0.34 will reach break even.

Key Takeaways from Altice’s Q1 Results

We struggled to find many positives in these results as its EPS and EBITDA missed significantly. Its number of broadband subscribers also fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 4.5% to $2.52 immediately following the results.

Altice may have had a tough quarter, but does that actually create an opportunity to invest right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.