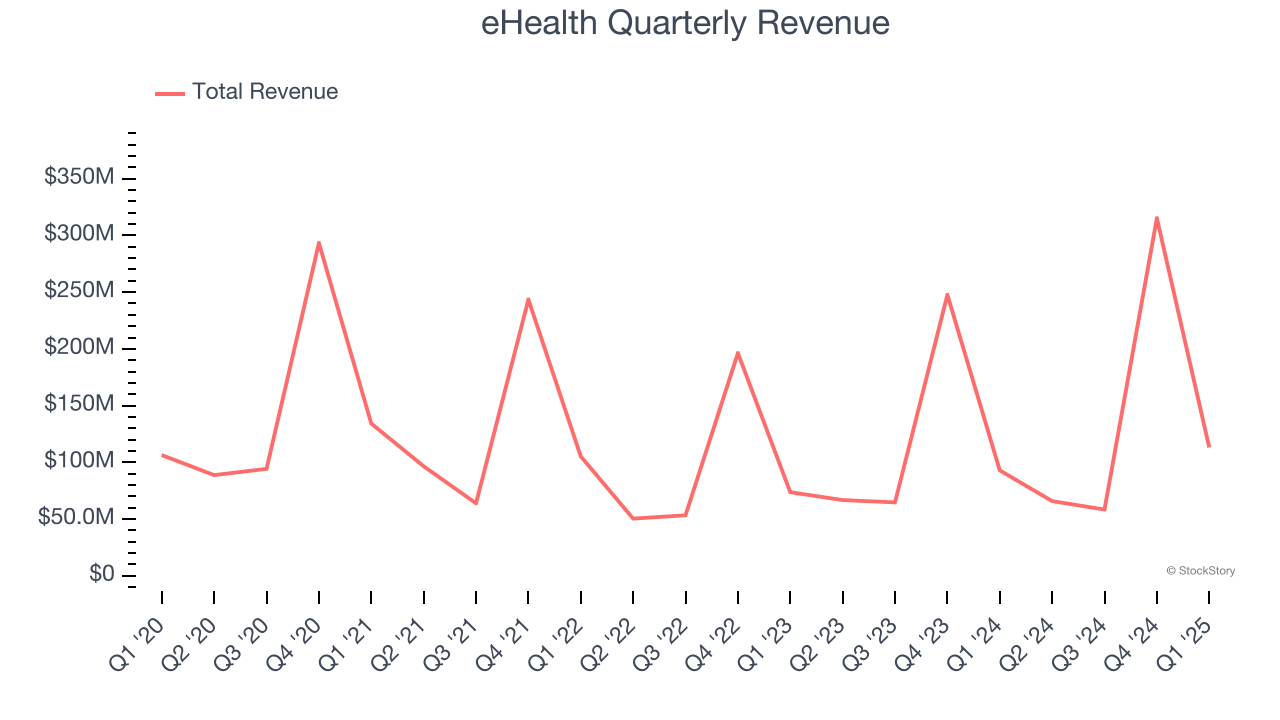

Online health insurance comparison site eHealth (NASDAQ: EHTH) beat Wall Street’s revenue expectations in Q1 CY2025, with sales up 21.7% year on year to $113.1 million. The company expects the full year’s revenue to be around $530 million, close to analysts’ estimates. Its GAAP loss of $0.33 per share was 56.6% above analysts’ consensus estimates.

Is now the time to buy eHealth? Find out by accessing our full research report, it’s free.

eHealth (EHTH) Q1 CY2025 Highlights:

- Revenue: $113.1 million vs analyst estimates of $99.72 million (21.7% year-on-year growth, 13.4% beat)

- EPS (GAAP): -$0.33 vs analyst estimates of -$0.76 (56.6% beat)

- Adjusted EBITDA: $12.52 million vs analyst estimates of -$7.99 million (11.1% margin, significant beat)

- The company reconfirmed its revenue guidance for the full year of $530 million at the midpoint

- EBITDA guidance for the full year is $47.5 million at the midpoint, above analyst estimates of $46.01 million

- Operating Margin: 4.2%, up from -19.3% in the same quarter last year

- Free Cash Flow was $73.7 million, up from -$30.99 million in the previous quarter

- Estimated Membership: 1.16 million, down 21,363 year on year

- Market Capitalization: $140.1 million

Company Overview

Aiming to address a high-stakes and often confusing decision, eHealth (NASDAQ: EHTH) guides consumers through health insurance enrollment and related topics.

Sales Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last three years, eHealth grew its sales at a sluggish 2.8% compounded annual growth rate. This was below our standards and is a rough starting point for our analysis.

This quarter, eHealth reported robust year-on-year revenue growth of 21.7%, and its $113.1 million of revenue topped Wall Street estimates by 13.4%.

Looking ahead, sell-side analysts expect revenue to decline by 2.3% over the next 12 months, a deceleration versus the last three years. This projection doesn't excite us and suggests its products and services will see some demand headwinds.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Estimated Membership

User Growth

As an online marketplace, eHealth generates revenue growth by increasing both the number of users on its platform and the average order size in dollars.

eHealth struggled with new customer acquisition over the last two years as its estimated membership have declined by 1.8% annually to 1.16 million in the latest quarter. This performance isn't ideal because internet usage is secular, meaning there are typically unaddressed market opportunities. If eHealth wants to accelerate growth, it likely needs to enhance the appeal of its current offerings or innovate with new products.

In Q1, eHealth’s estimated membership once again decreased by 21,363, a 1.8% drop since last year. The quarterly print isn’t too different from its two-year result, suggesting its new initiatives aren’t accelerating user growth just yet.

Revenue Per User

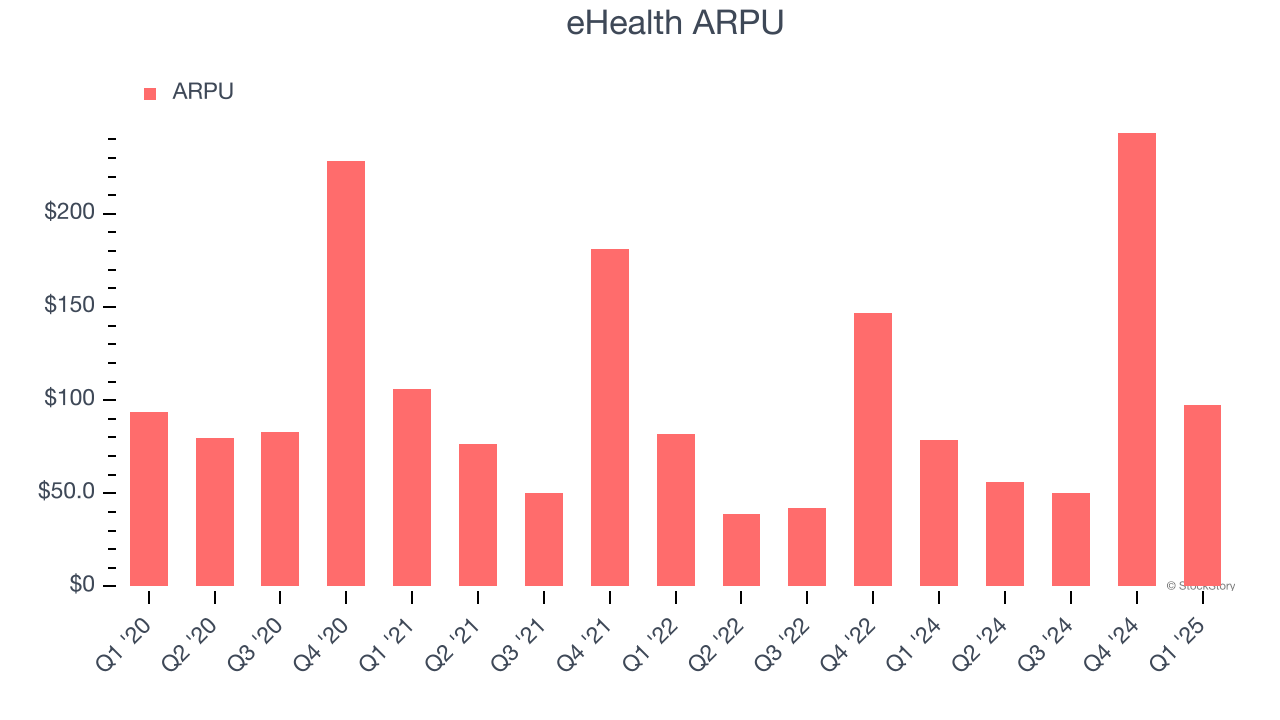

Average revenue per user (ARPU) is a critical metric to track because it measures how much the company earns in transaction fees from each user. ARPU also gives us unique insights into a user’s average order size and eHealth’s take rate, or "cut", on each order.

eHealth’s ARPU growth has been exceptional over the last two years, averaging 23.9%. Although its estimated membership shrank during this time, the company’s ability to successfully increase monetization demonstrates its platform’s value for existing users.

This quarter, eHealth’s ARPU clocked in at $97.63. It grew by 23.9% year on year, faster than its estimated membership.

Key Takeaways from eHealth’s Q1 Results

We were impressed by how significantly eHealth blew past analysts’ revenue, EPS, and EBITDA expectations this quarter. We were also glad its full-year EBITDA guidance topped Wall Street's estimates. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 15.5% to $5.40 immediately following the results.

Indeed, eHealth had a rock-solid quarterly earnings result, but is this stock a good investment here? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.