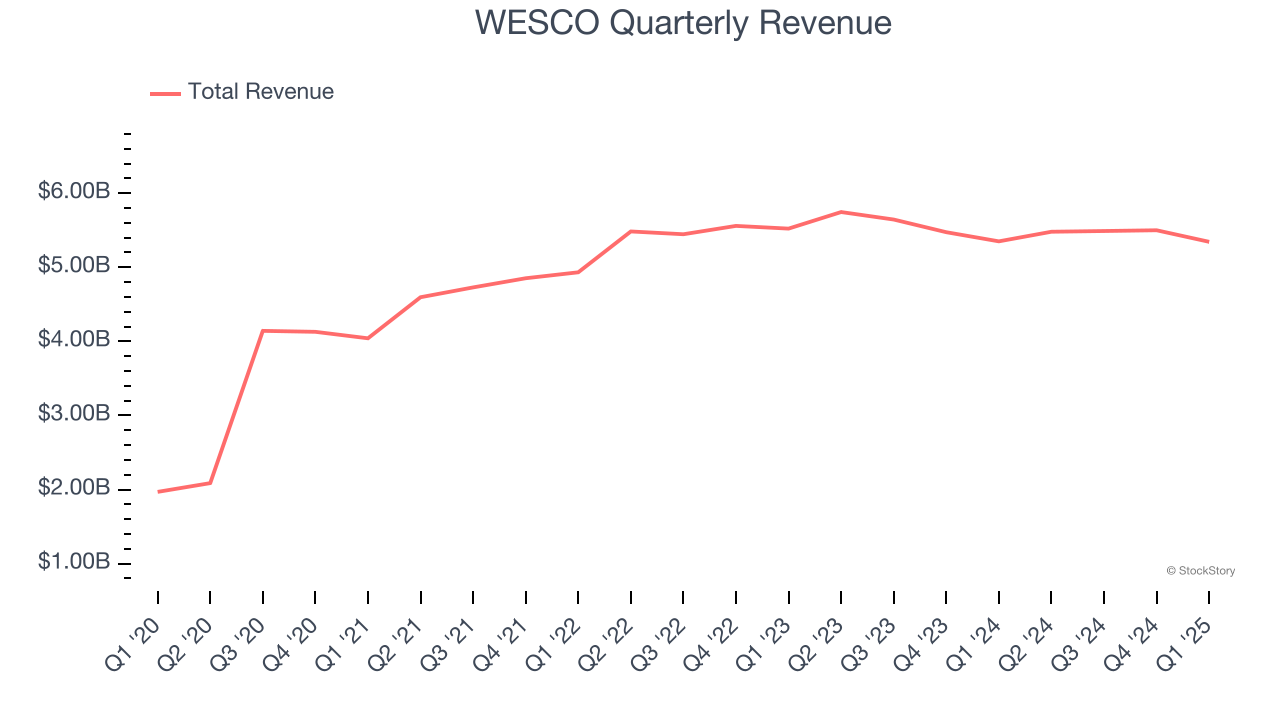

Electrical supply company WESCO (NYSE: WCC) reported Q1 CY2025 results beating Wall Street’s revenue expectations, but sales were flat year on year at $5.34 billion. Its non-GAAP profit of $2.21 per share was 4.7% below analysts’ consensus estimates.

Is now the time to buy WESCO? Find out by accessing our full research report, it’s free.

WESCO (WCC) Q1 CY2025 Highlights:

- Revenue: $5.34 billion vs analyst estimates of $5.25 billion (flat year on year, 1.8% beat)

- Adjusted EPS: $2.21 vs analyst expectations of $2.32 (4.7% miss)

- Adjusted EBITDA: $310.7 million vs analyst estimates of $323 million (5.8% margin, 3.8% miss)

- Operating Margin: 4.5%, in line with the same quarter last year

- Free Cash Flow Margin: 0.1%, down from 13.7% in the same quarter last year

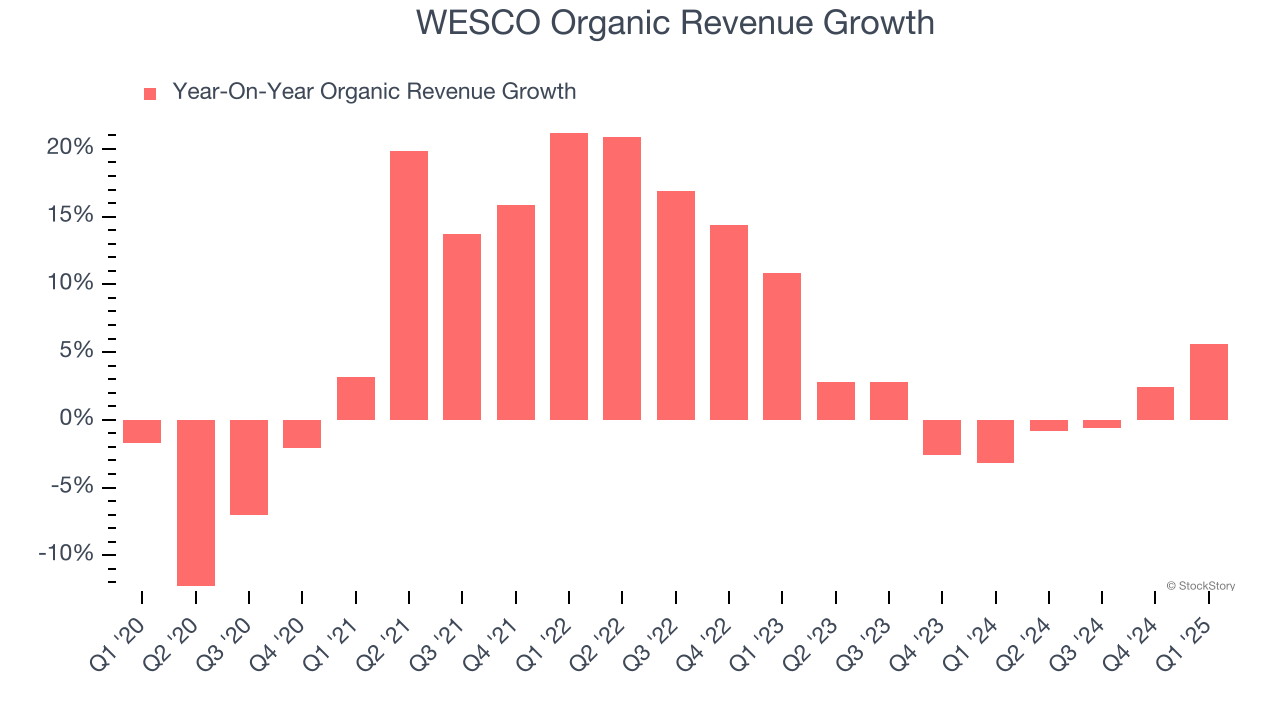

- Organic Revenue rose 5.6% year on year (-3.2% in the same quarter last year)

- Market Capitalization: $7.95 billion

"After returning to growth in the fourth quarter of 2024, we are pleased to build on our positive sales momentum to start the year with 6% organic growth in the first quarter. This performance was sparked by 70% growth in total data center sales and high single digit growth in both our Broadband and OEM businesses. Consistent with the fourth quarter, our first quarter sales growth was partially offset by continued weakness in our utility business, as expected. With that said, our positive momentum is building to start the second quarter with preliminary April sales per workday up 7% versus prior year. Our opportunity pipeline continues at a record level, bid activity levels remain very strong, and backlog is growing. Gross margin was relatively stable on a sequential basis versus the fourth quarter, and we've begun to see an initial improvement in Communication and Security Solutions as expected," said John Engel, Chairman, President, and CEO.

Company Overview

Based in Pittsburgh, WESCO (NYSE: WCC) provides electrical, industrial, and communications products and augments them with services such as supply chain management.

Sales Growth

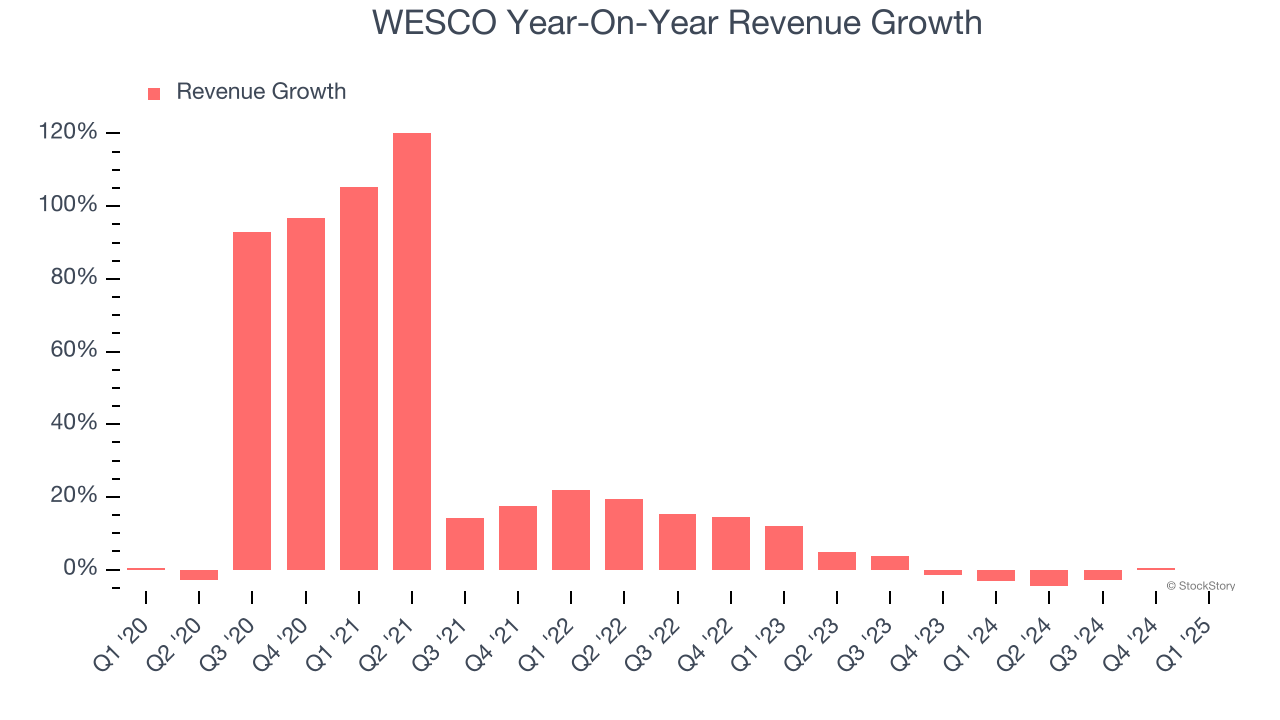

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, WESCO’s 21.1% annualized revenue growth over the last five years was incredible. Its growth beat the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. WESCO’s recent performance shows its demand has slowed significantly as its revenue was flat over the last two years.

We can dig further into the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, WESCO’s organic revenue was flat. Because this number aligns with its normal revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, WESCO’s $5.34 billion of revenue was flat year on year but beat Wall Street’s estimates by 1.8%.

Looking ahead, sell-side analysts expect revenue to grow 3.5% over the next 12 months. While this projection suggests its newer products and services will catalyze better top-line performance, it is still below average for the sector.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

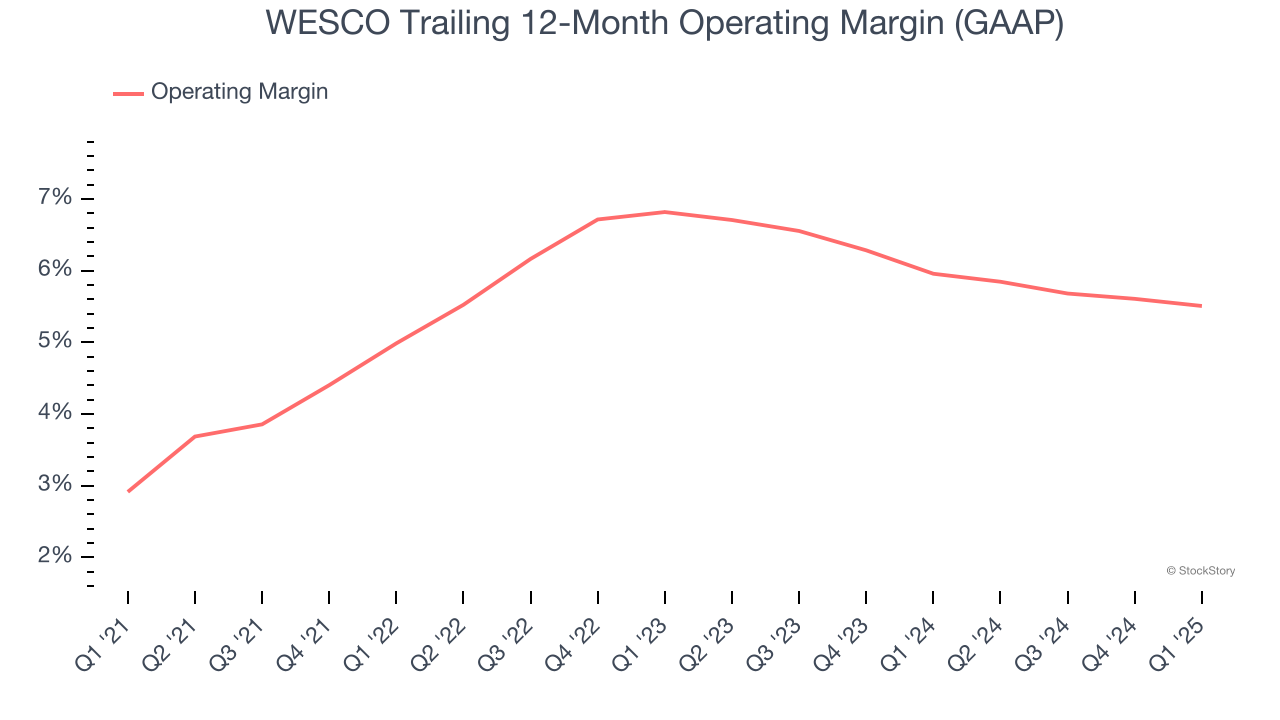

WESCO was profitable over the last five years but held back by its large cost base. Its average operating margin of 5.4% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

On the plus side, WESCO’s operating margin rose by 2.6 percentage points over the last five years, as its sales growth gave it operating leverage.

This quarter, WESCO generated an operating profit margin of 4.5%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

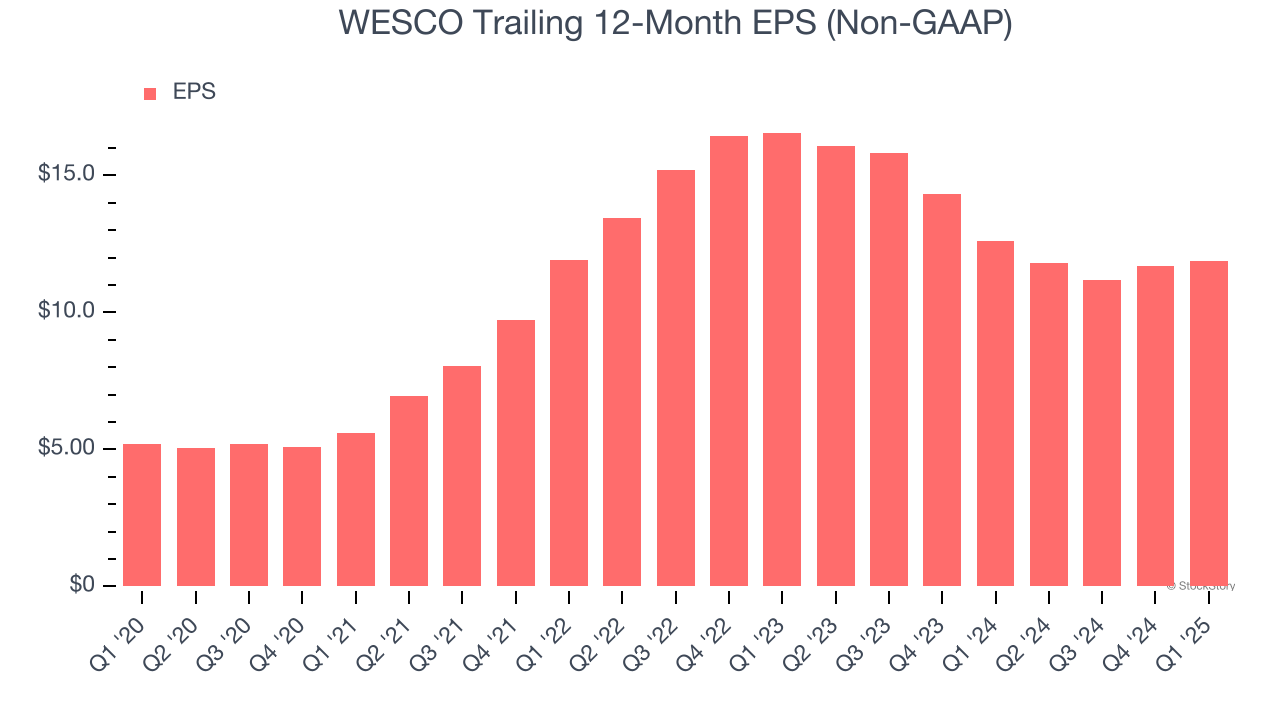

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

WESCO’s EPS grew at an astounding 18% compounded annual growth rate over the last five years. Despite its operating margin expansion during that time, this performance was lower than its 21.1% annualized revenue growth, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

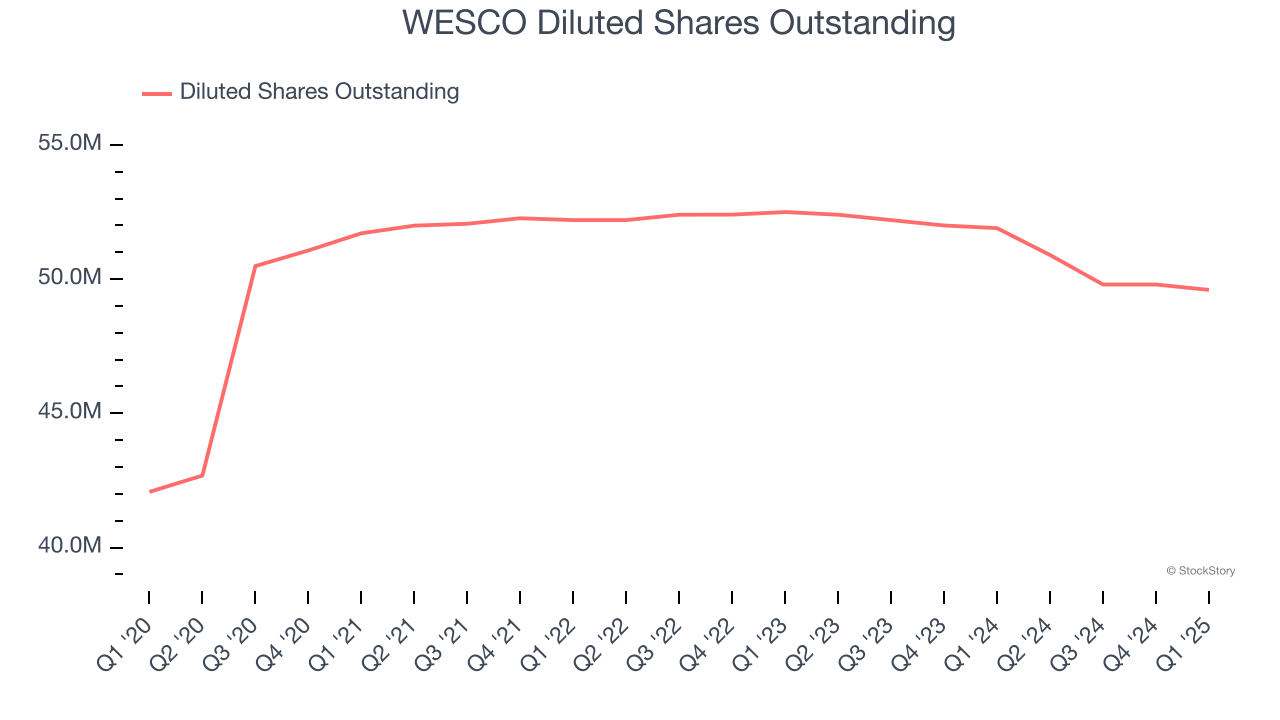

Diving into WESCO’s quality of earnings can give us a better understanding of its performance. A five-year view shows WESCO has diluted its shareholders, growing its share count by 17.9%. This dilution overshadowed its increased operating efficiency and has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For WESCO, its two-year annual EPS declines of 15.3% mark a reversal from its (seemingly) healthy five-year trend. We hope WESCO can return to earnings growth in the future.

In Q1, WESCO reported EPS at $2.21, up from $2.02 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects WESCO’s full-year EPS of $11.88 to grow 19.5%.

Key Takeaways from WESCO’s Q1 Results

We enjoyed seeing WESCO beat analysts’ organic revenue expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. On the other hand, its EPS missed and its EBITDA fell short of Wall Street’s estimates. Zooming out, we think this was a mixed quarter. The stock remained flat at $163.46 immediately following the results.

Is WESCO an attractive investment opportunity right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.