SmartRent’s stock price has taken a beating over the past six months, shedding 41.8% of its value and falling to a new 52-week low of $0.96 per share. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Following the pullback, is now an opportune time to buy SMRT? Find out in our full research report, it’s free.

Why Does SmartRent Spark Debate?

Founded by an employee at a real estate rental company, SmartRent (NYSE: SMRT) provides smart home devices and software for multifamily residential properties, single-family rental homes, and student housing communities.

Two Things to Like:

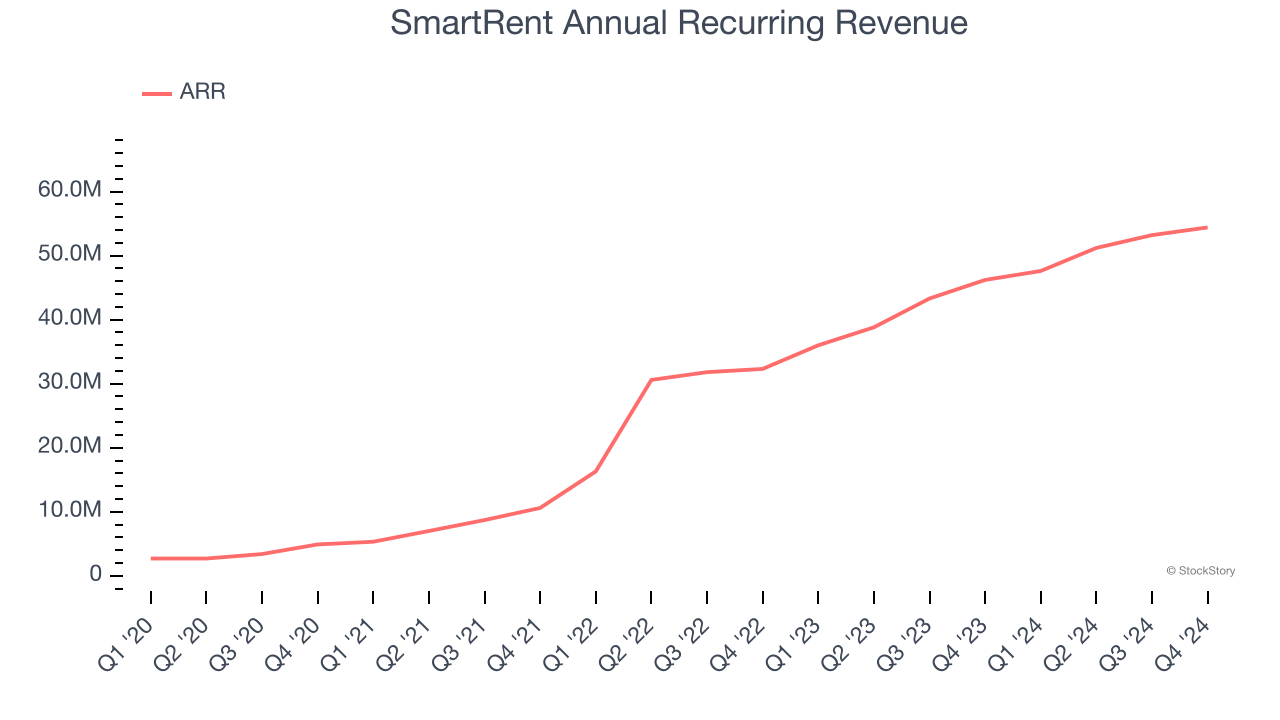

1. ARR Surges as Recurring Revenue Flows In

We can better understand Internet of Things companies by analyzing their ARR, or annual recurring revenue. This metric shows how much SmartRent expects to collect from its existing customer base in the next 12 months, giving visibility into its future revenue streams.

SmartRent’s ARR punched in at $54.4 million in the latest quarter, and over the last two years, its year-on-year growth averaged 41.5%. This performance was fantastic and shows that customers are willing to take multi-year bets on the company’s product offerings. Its growth also makes SmartRent a more predictable business, a tailwind for its valuation as investors typically prefer businesses with recurring revenue.

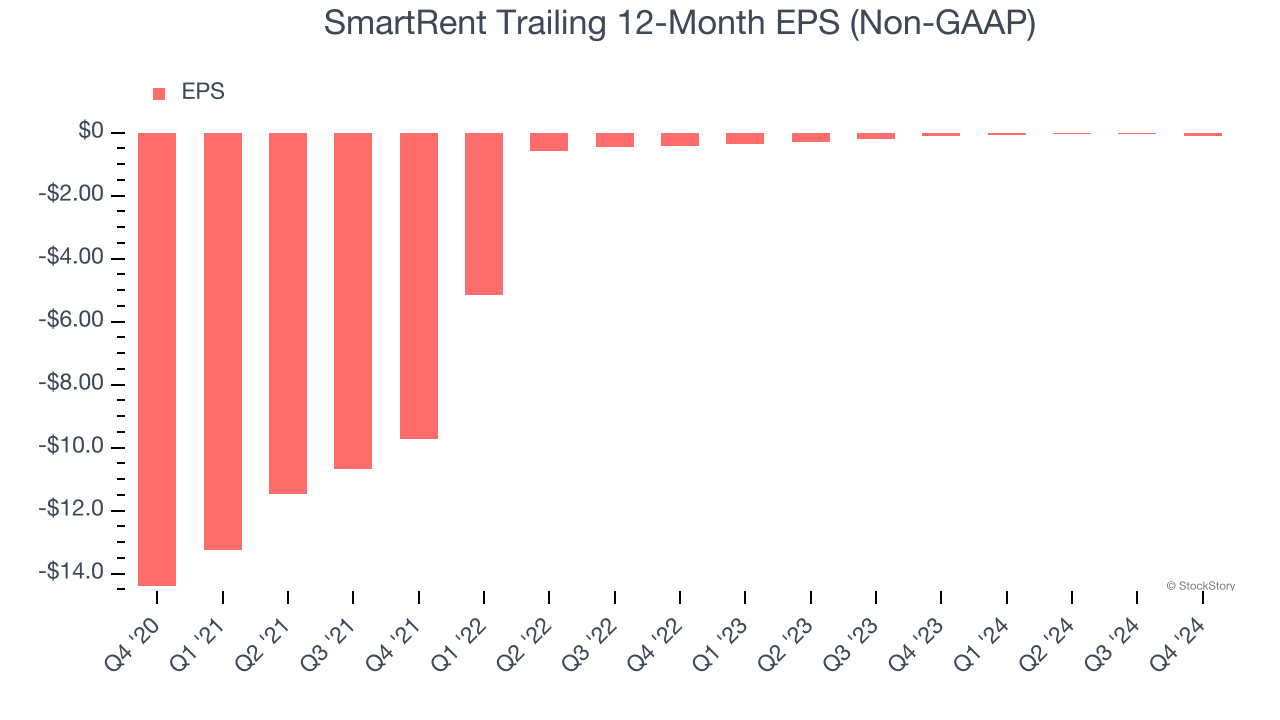

2. EPS Improving Significantly

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Although SmartRent’s full-year earnings are still negative, it reduced its losses and improved its EPS by 71.2% annually over the last four years. The next few quarters will be critical for assessing its long-term profitability. We hope to see an inflection point soon.

One Reason to be Careful:

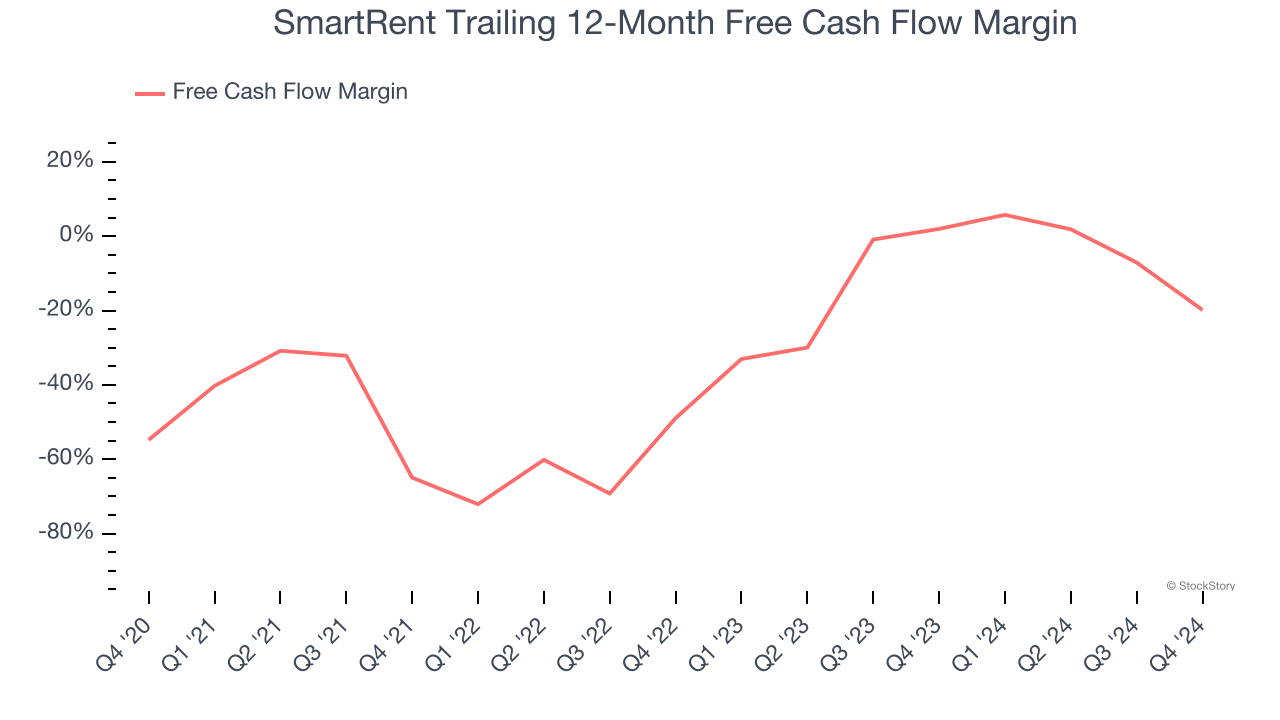

Cash Burn Ignites Concerns

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

SmartRent’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 28.6%, meaning it lit $28.65 of cash on fire for every $100 in revenue.

Final Judgment

SmartRent has huge potential even though it has some open questions. After the recent drawdown, the stock trades at $0.96 per share (or 1.2× forward price-to-sales). Is now a good time to initiate a position? See for yourself in our comprehensive research report, it’s free.

Stocks We Like Even More Than SmartRent

Market indices reached historic highs following Donald Trump’s presidential victory in November 2024, but the outlook for 2025 is clouded by new trade policies that could impact business confidence and growth.

While this has caused many investors to adopt a "fearful" wait-and-see approach, we’re leaning into our best ideas that can grow regardless of the political or macroeconomic climate. Take advantage of Mr. Market by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.