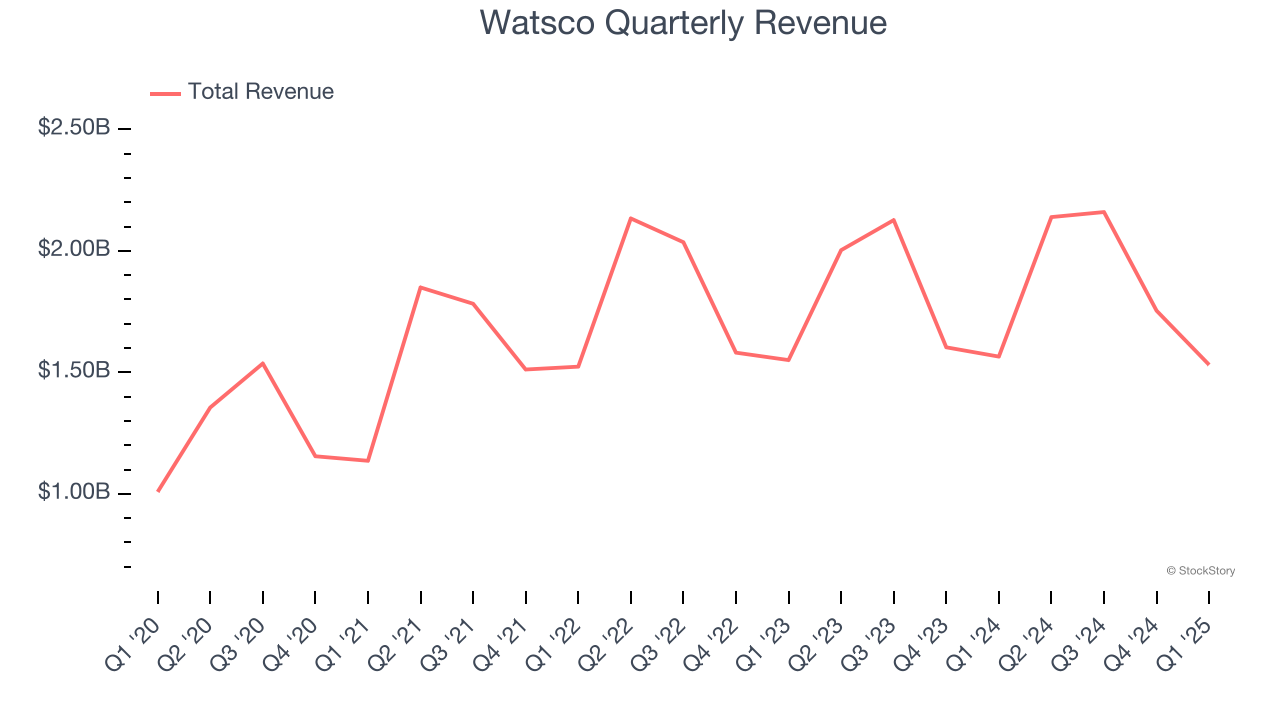

Equipment distributor Watsco (NYSE: WSO) fell short of the market’s revenue expectations in Q1 CY2025, with sales falling 2.2% year on year to $1.53 billion. Its GAAP profit of $1.93 per share was 14.1% below analysts’ consensus estimates.

Is now the time to buy Watsco? Find out by accessing our full research report, it’s free.

Watsco (WSO) Q1 CY2025 Highlights:

- Revenue: $1.53 billion vs analyst estimates of $1.65 billion (2.2% year-on-year decline, 7.3% miss)

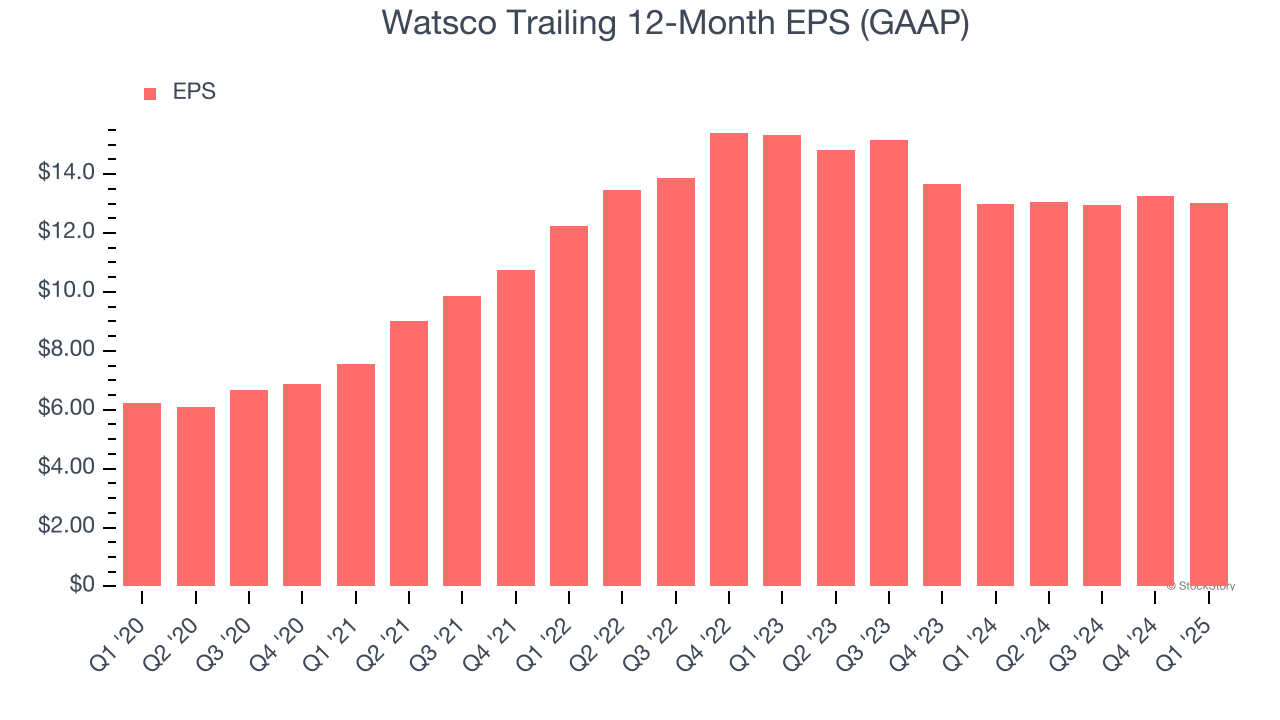

- EPS (GAAP): $1.93 vs analyst expectations of $2.25 (14.1% miss)

- Adjusted EBITDA: $131.8 million vs analyst estimates of $143.7 million (8.6% margin, 8.3% miss)

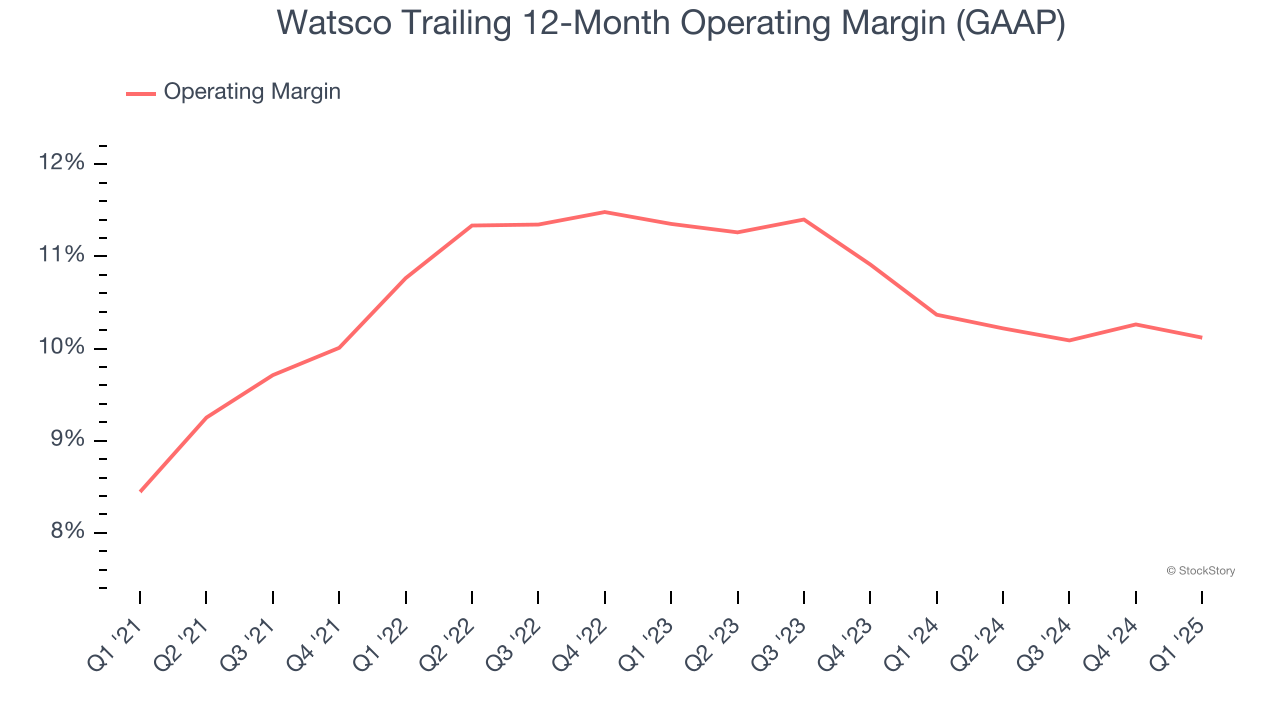

- Operating Margin: 7.3%, in line with the same quarter last year

- Free Cash Flow was -$185.1 million, down from $97.92 million in the same quarter last year

- Market Capitalization: $19.03 billion

Company Overview

Originally a manufacturing company, Watsco (NYSE: WSO) today only distributes air conditioning, heating, and refrigeration equipment, as well as related parts and supplies.

Infrastructure Distributors

Focusing on narrow product categories that can lead to economies of scale, infrastructure distributors sell essential goods that often enjoy more predictable revenue streams. For example, the ongoing inspection, maintenance, and replacement of pipes and water pumps are critical to a functioning society, rendering them non-discretionary. Lately, innovation to address trends like water conservation has driven incremental sales. But like the broader industrials sector, infrastructure distributors are also at the whim of economic cycles as external factors like interest rates can greatly impact commercial and residential construction projects that drive demand for infrastructure products.

Sales Growth

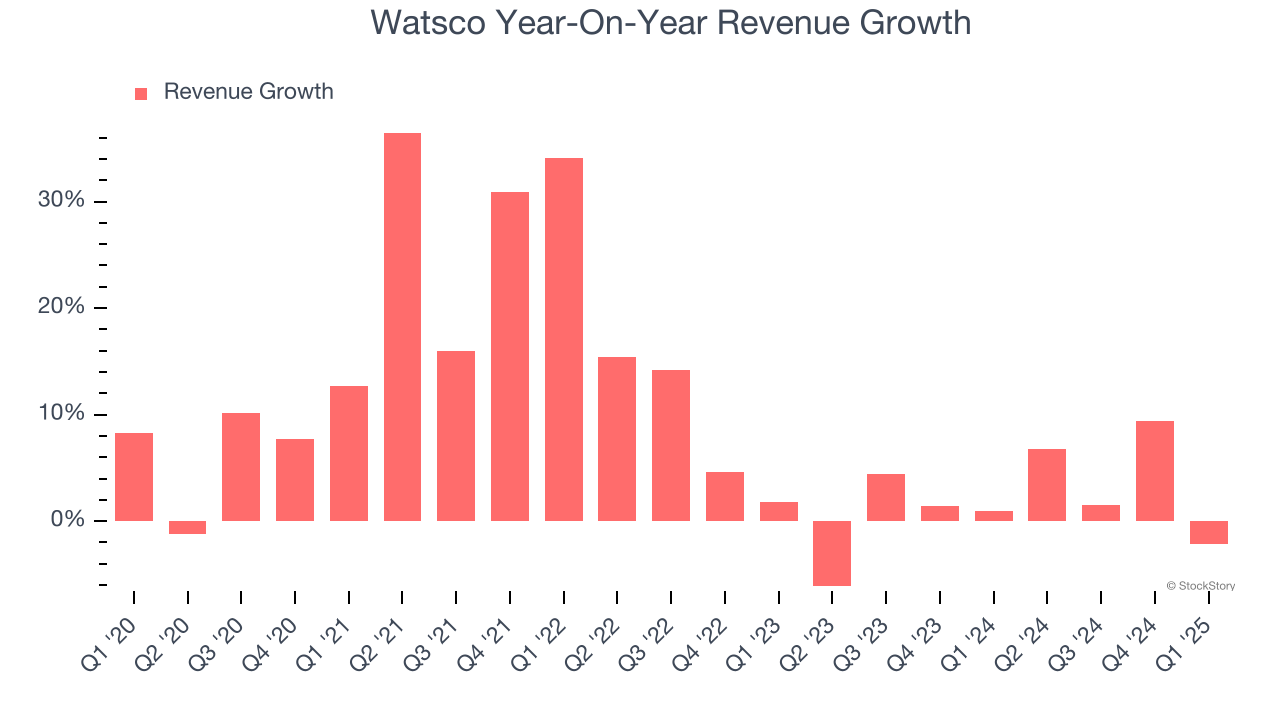

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Thankfully, Watsco’s 9.4% annualized revenue growth over the last five years was solid. Its growth beat the average industrials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Watsco’s recent performance shows its demand has slowed as its annualized revenue growth of 1.9% over the last two years was below its five-year trend.

This quarter, Watsco missed Wall Street’s estimates and reported a rather uninspiring 2.2% year-on-year revenue decline, generating $1.53 billion of revenue.

Looking ahead, sell-side analysts expect revenue to grow 8% over the next 12 months, an improvement versus the last two years. This projection is above average for the sector and suggests its newer products and services will fuel better top-line performance.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Watsco has managed its cost base well over the last five years. It demonstrated solid profitability for an industrials business, producing an average operating margin of 10.3%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Looking at the trend in its profitability, Watsco’s operating margin rose by 1.7 percentage points over the last five years, as its sales growth gave it operating leverage.

This quarter, Watsco generated an operating profit margin of 7.3%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Watsco’s EPS grew at a spectacular 15.8% compounded annual growth rate over the last five years, higher than its 9.4% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Diving into Watsco’s quality of earnings can give us a better understanding of its performance. As we mentioned earlier, Watsco’s operating margin was flat this quarter but expanded by 1.7 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Watsco, its two-year annual EPS declines of 7.9% mark a reversal from its (seemingly) healthy five-year trend. We hope Watsco can return to earnings growth in the future.

In Q1, Watsco reported EPS at $1.93, down from $2.17 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects Watsco’s full-year EPS of $13.01 to grow 15.7%.

Key Takeaways from Watsco’s Q1 Results

We struggled to find many positives in these results. Its revenue missed significantly and its EBITDA fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 4% to $484 immediately after reporting.

Watsco’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.