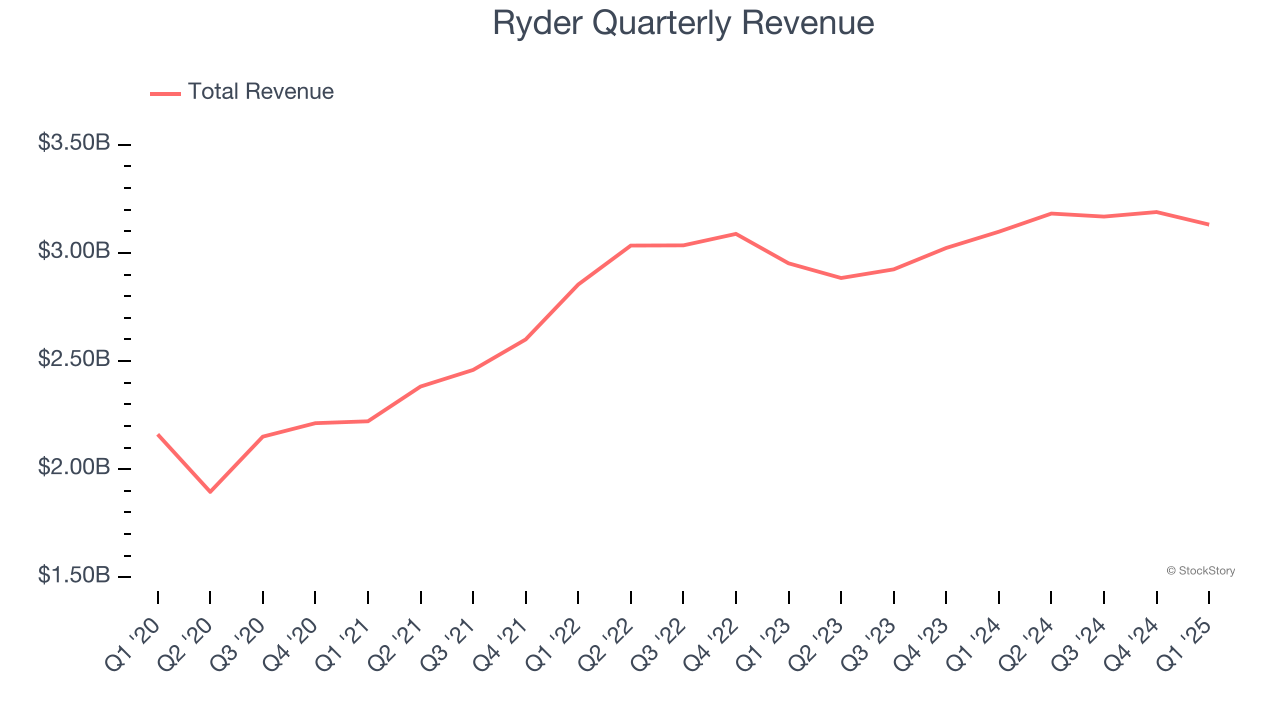

Commercial rental vehicle and delivery company Ryder (NYSE: R) met Wall Street’s revenue expectations in Q1 CY2025, with sales up 1.1% year on year to $3.13 billion. Its GAAP profit of $2.27 per share was 0.6% above analysts’ consensus estimates.

Is now the time to buy Ryder? Find out by accessing our full research report, it’s free.

Ryder (R) Q1 CY2025 Highlights:

- Revenue: $3.13 billion vs analyst estimates of $3.14 billion (1.1% year-on-year growth, in line)

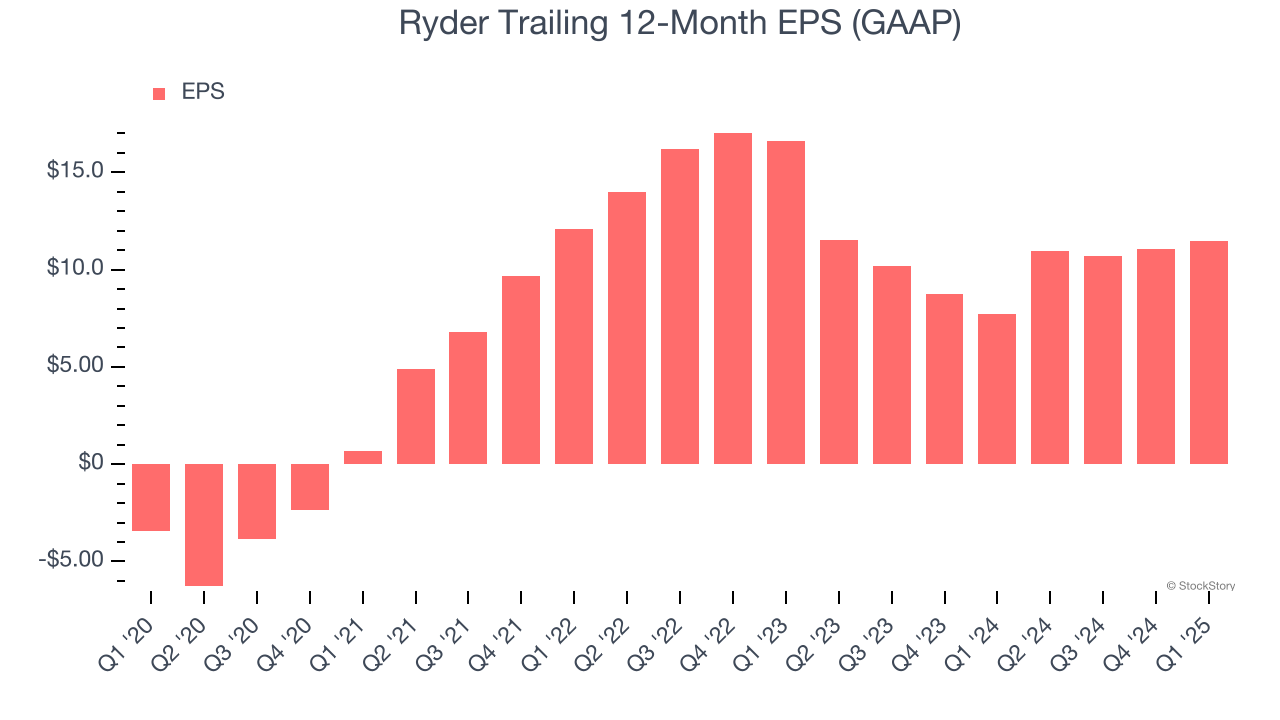

- EPS (GAAP): $2.27 vs analyst estimates of $2.26 (0.6% beat)

- Adjusted EBITDA: $671 million vs analyst estimates of $656 million (21.4% margin, 2.3% beat)

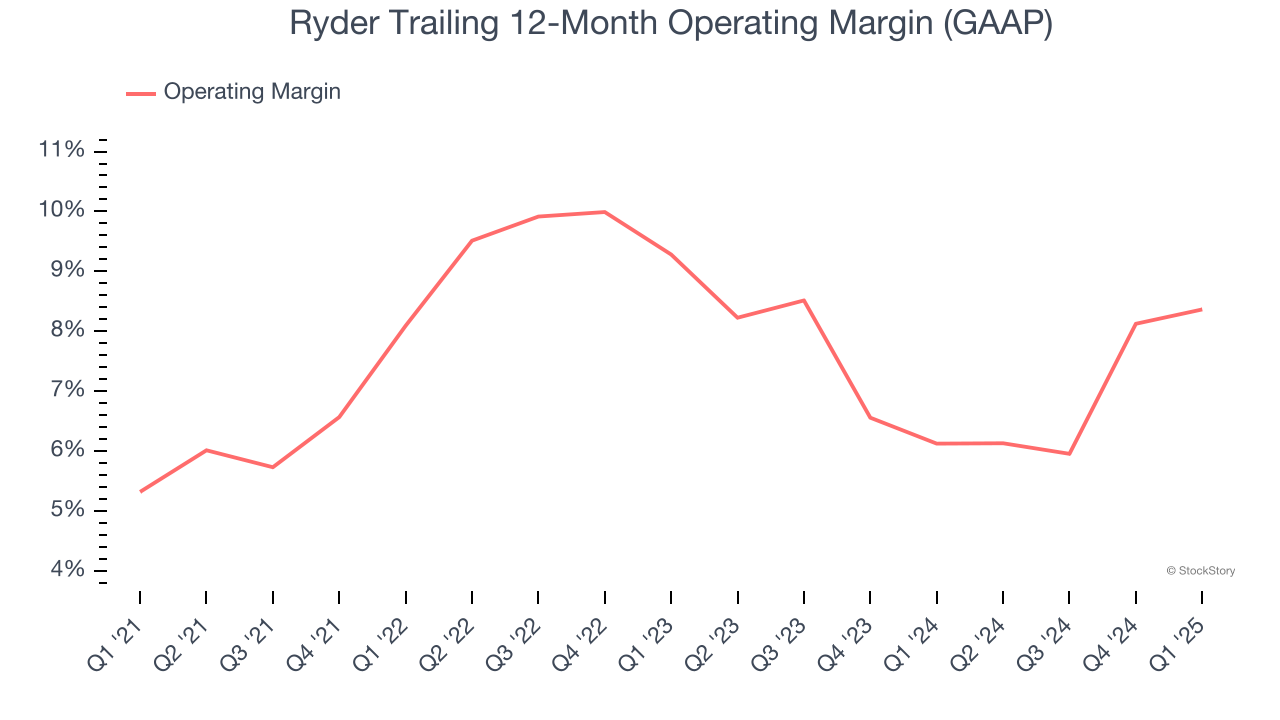

- Operating Margin: 7.6%, in line with the same quarter last year

- Free Cash Flow was $259 million, up from -$160 million in the same quarter last year

- Market Capitalization: $5.76 billion

"I'm proud of the Ryder team for delivering double-digit earnings growth in the first quarter," says Ryder Chairman and CEO Robert Sanchez.

Company Overview

As one of the first companies to introduce the idea of leasing trucks, Ryder (NYSE: R) provides rental vehicles to businesses and delivers packages directly to homes or businesses.

Ground Transportation

The growth of e-commerce and global trade continues to drive demand for shipping services, especially last-mile delivery, presenting opportunities for ground transportation companies. The industry continues to invest in data, analytics, and autonomous fleets to optimize efficiency and find the most cost-effective routes. Despite the essential services this industry provides, ground transportation companies are still at the whim of economic cycles. Consumer spending, for example, can greatly impact the demand for these companies’ offerings while fuel costs can influence profit margins.

Sales Growth

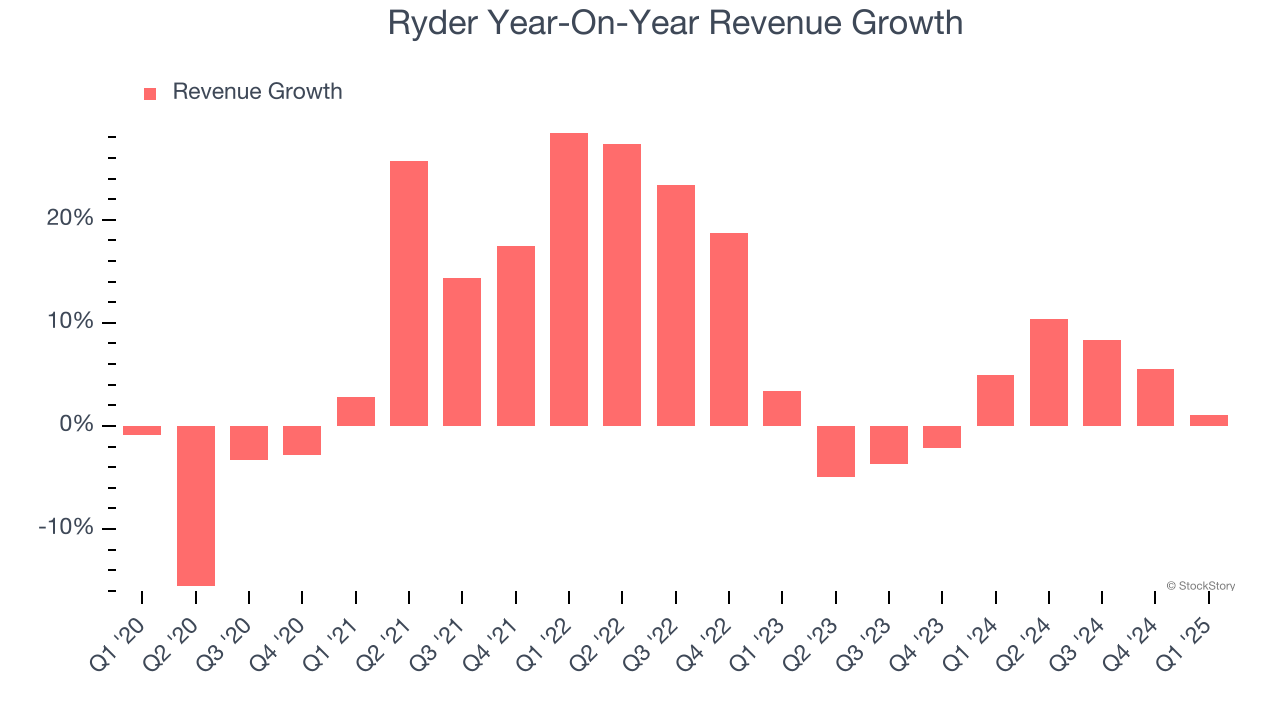

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, Ryder’s 7.3% annualized revenue growth over the last five years was mediocre. This fell short of our benchmark for the industrials sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Ryder’s recent performance shows its demand has slowed as its annualized revenue growth of 2.3% over the last two years was below its five-year trend. We also note many other Ground Transportation businesses have faced declining sales because of cyclical headwinds. While Ryder grew slower than we’d like, it did do better than its peers.

We can dig further into the company’s revenue dynamics by analyzing its most important segments, Fleet Management Solutions and Supply Chain Solutions, which are 46.2% and 42.5% of revenue. Over the last two years, Ryder’s Fleet Management Solutions revenue (leasing and rental) averaged 3.3% year-on-year declines. On the other hand, its Supply Chain Solutions revenue ( designing and managing customers' distribution) averaged 5.1% growth.

This quarter, Ryder grew its revenue by 1.1% year on year, and its $3.13 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 2.7% over the next 12 months, similar to its two-year rate. This projection is underwhelming and suggests its newer products and services will not catalyze better top-line performance yet.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Ryder was profitable over the last five years but held back by its large cost base. Its average operating margin of 7.6% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

On the plus side, Ryder’s operating margin rose by 3 percentage points over the last five years, as its sales growth gave it operating leverage.

This quarter, Ryder generated an operating profit margin of 7.6%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Ryder’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

Sadly for Ryder, its EPS declined by 16.9% annually over the last two years while its revenue grew by 2.3%. This tells us the company became less profitable on a per-share basis as it expanded.

In Q1, Ryder reported EPS at $2.27, up from $1.89 in the same quarter last year. This print was close to analysts’ estimates. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from Ryder’s Q1 Results

It was encouraging to see Ryder beat analysts’ EBITDA and EPS expectations this quarter. On the other hand, its revenue was just in line. Zooming out, we think this was a mixed quarter. The stock remained flat at $138 immediately after reporting.

Is Ryder an attractive investment opportunity at the current price? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.