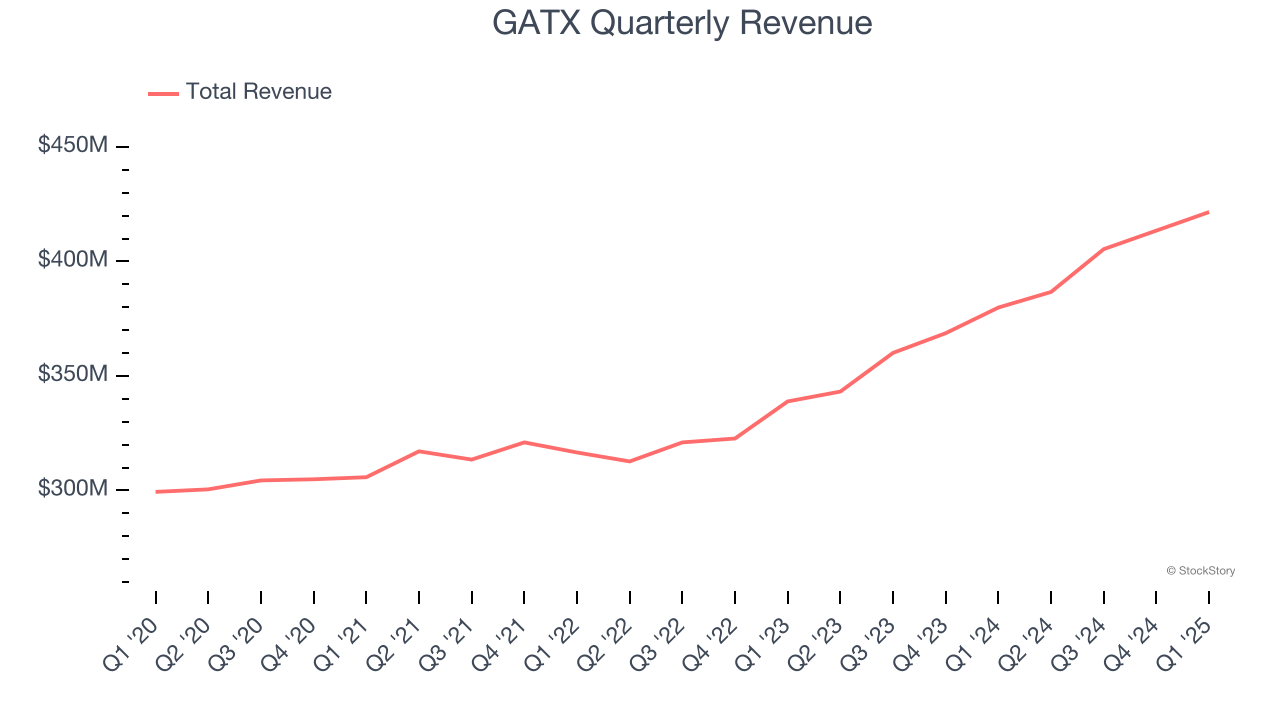

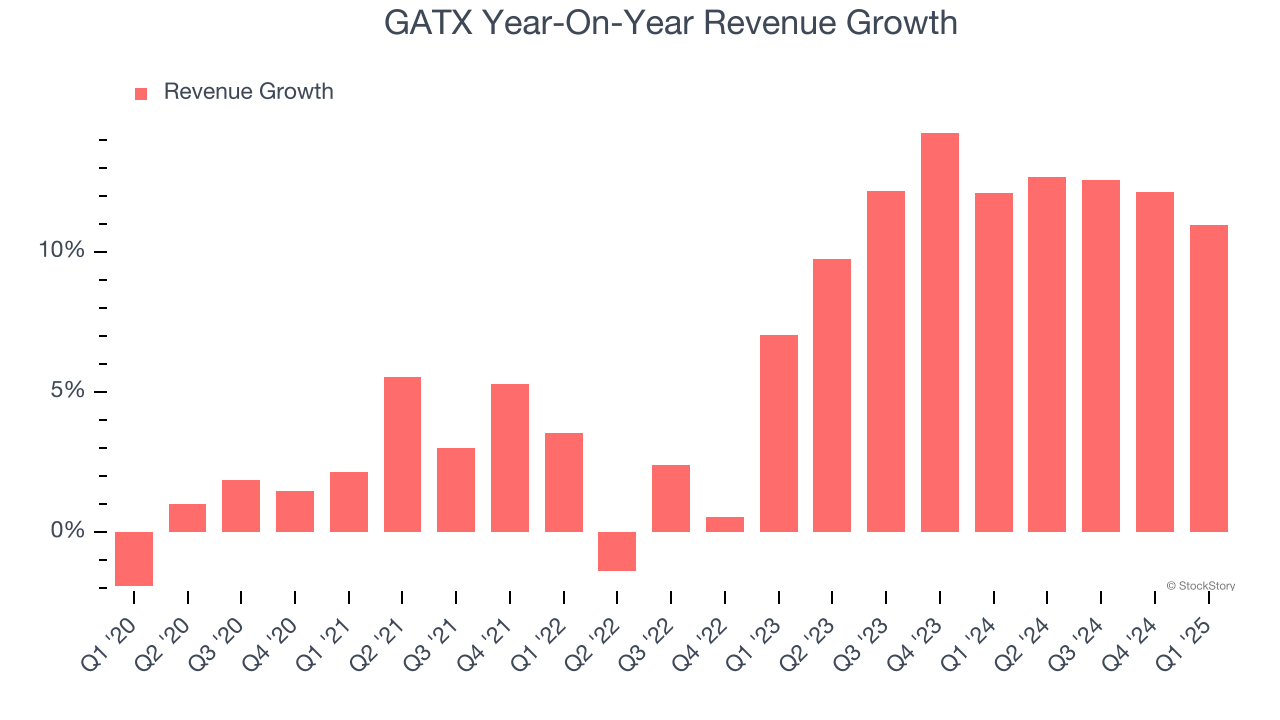

Leasing services company GATX (NYSE: GATX) announced better-than-expected revenue in Q1 CY2025, with sales up 11% year on year to $421.6 million. Its non-GAAP profit of $2.15 per share was 3% above analysts’ consensus estimates.

Is now the time to buy GATX? Find out by accessing our full research report, it’s free.

GATX (GATX) Q1 CY2025 Highlights:

- Revenue: $421.6 million vs analyst estimates of $417.1 million (11% year-on-year growth, 1.1% beat)

- Adjusted EPS: $2.15 vs analyst estimates of $2.09 (3% beat)

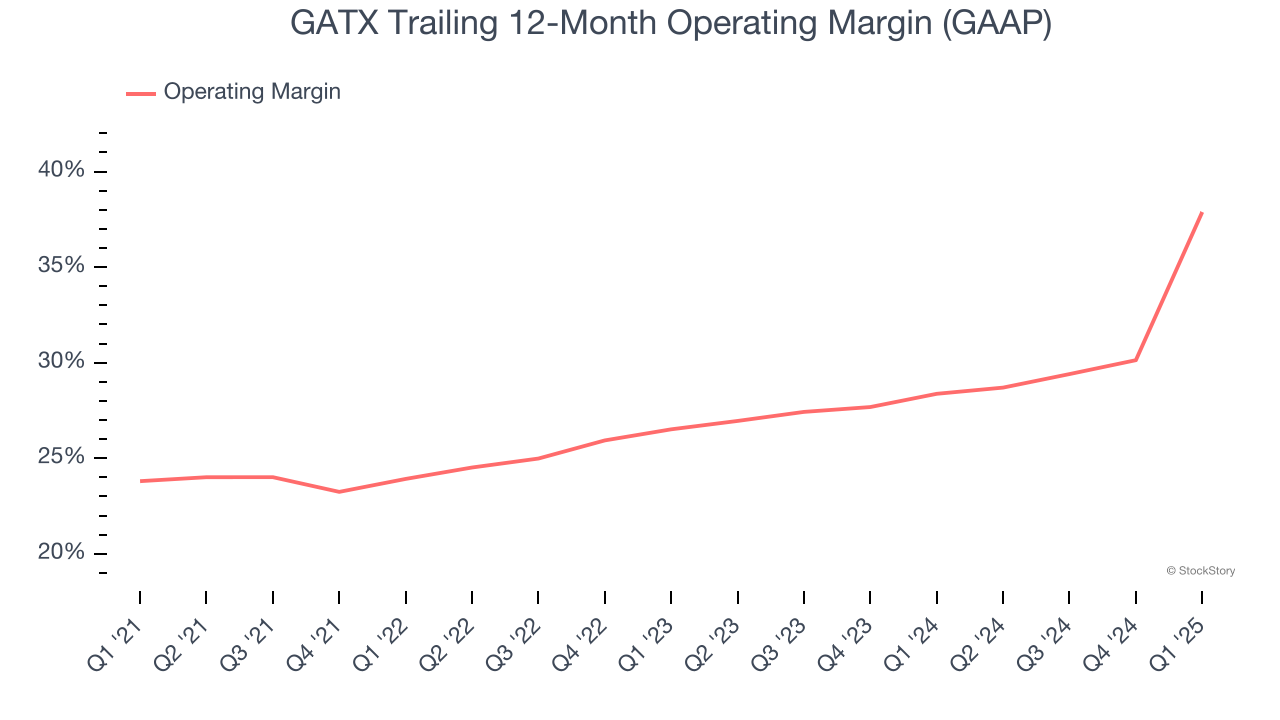

- Operating Margin: 60.2%, up from 30.3% in the same quarter last year

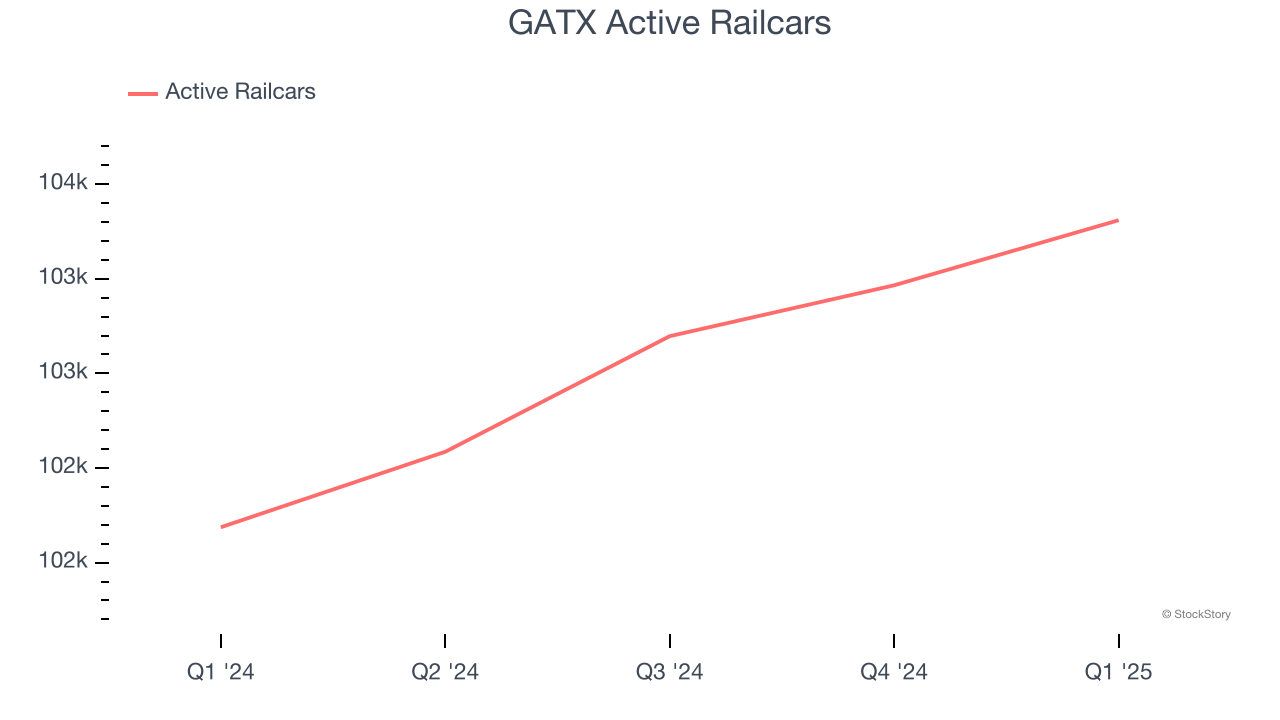

- Active Railcars: 103,310, up 1,623 year on year

- Market Capitalization: $5.30 billion

Company Overview

Originally founded to ship beer, GATX (NYSE: GATX) provides leasing and management services for railcars and other transportation assets globally.

Vehicle Parts Distributors

Supply chain and inventory management are themes that grew in focus after COVID wreaked havoc on the global movement of raw materials and components. Transportation parts distributors that boast reliable selection in sometimes specialized areas combined and quickly deliver products to customers can benefit from this theme. Additionally, distributors who earn meaningful revenue streams from aftermarket products can enjoy more steady top-line trends and higher margins. But like the broader industrials sector, transportation parts distributors are also at the whim of economic cycles that impact capital spending, transportation volumes, and demand for discretionary parts and components.

Sales Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, GATX’s 6.3% annualized revenue growth over the last five years was mediocre. This fell short of our benchmark for the industrials sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. GATX’s annualized revenue growth of 12.1% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

We can better understand the company’s revenue dynamics by analyzing its number of active railcars, which reached 103,310 in the latest quarter. Over the last two years, GATX’s active railcars averaged 1.6% year-on-year growth. Because this number is lower than its revenue growth during the same period, we can see the company’s monetization has risen.

This quarter, GATX reported year-on-year revenue growth of 11%, and its $421.6 million of revenue exceeded Wall Street’s estimates by 1.1%.

Looking ahead, sell-side analysts expect revenue to grow 6.7% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and implies its products and services will see some demand headwinds.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

GATX has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 28.6%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, GATX’s operating margin rose by 14.1 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q1, GATX generated an operating profit margin of 60.2%, up 29.9 percentage points year on year. The increase was solid, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

Earnings Per Share

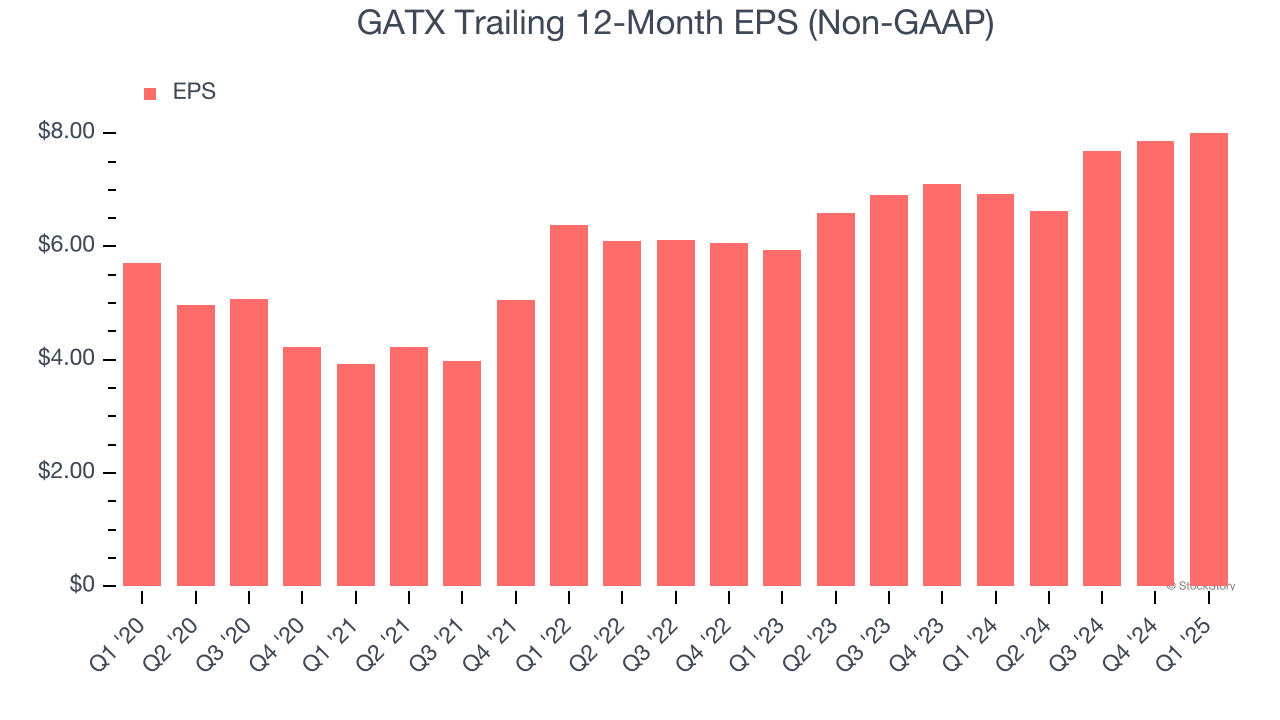

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

GATX’s unimpressive 7% annual EPS growth over the last five years aligns with its revenue performance. On the bright side, this tells us its incremental sales were profitable.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

GATX’s two-year annual EPS growth of 16.2% was great and topped its 12.1% two-year revenue growth.

In Q1, GATX reported EPS at $2.15, up from $2.01 in the same quarter last year. This print beat analysts’ estimates by 3%. Over the next 12 months, Wall Street expects GATX’s full-year EPS of $8.01 to grow 12.8%.

Key Takeaways from GATX’s Q1 Results

It was good to see GATX narrowly top analysts’ revenue expectations this quarter. We were also happy its EPS outperformed Wall Street’s estimates. Overall, this quarter had some key positives. The stock traded up 1% to $149.66 immediately following the results.

GATX had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.