While the broader market has struggled with the S&P 500 down 10.7% since October 2024, Rush Street Interactive has surged ahead as its stock price has climbed by 6.6% to $11.43 per share. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is there a buying opportunity in Rush Street Interactive, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Despite the momentum, we're sitting this one out for now. Here are two reasons why there are better opportunities than RSI and a stock we'd rather own.

Why Is Rush Street Interactive Not Exciting?

Specializing in online casino gaming and sports betting, Rush Street Interactive (NYSE: RSI) is an operator of digital gaming platforms.

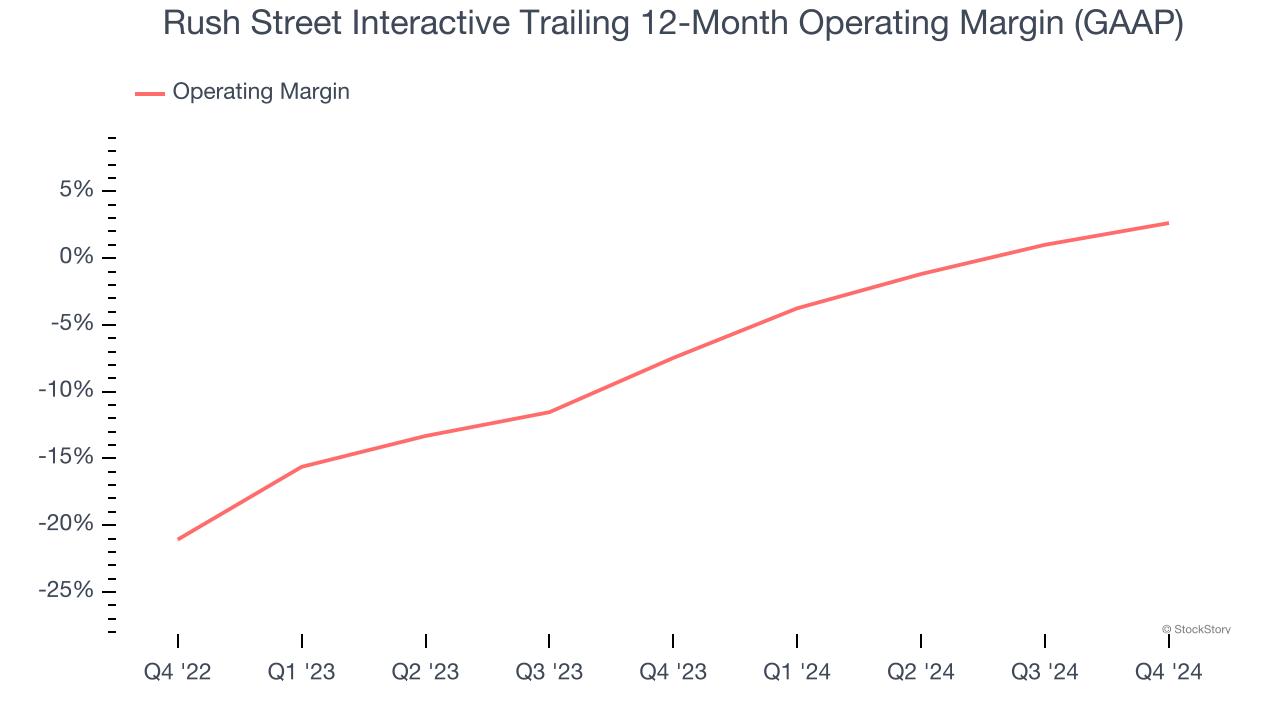

1. Operating Losses Sound the Alarms

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Rush Street Interactive’s operating margin has been trending up over the last 12 months, but it still averaged negative 1.7% over the last two years. This is due to its large expense base and inefficient cost structure.

2. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

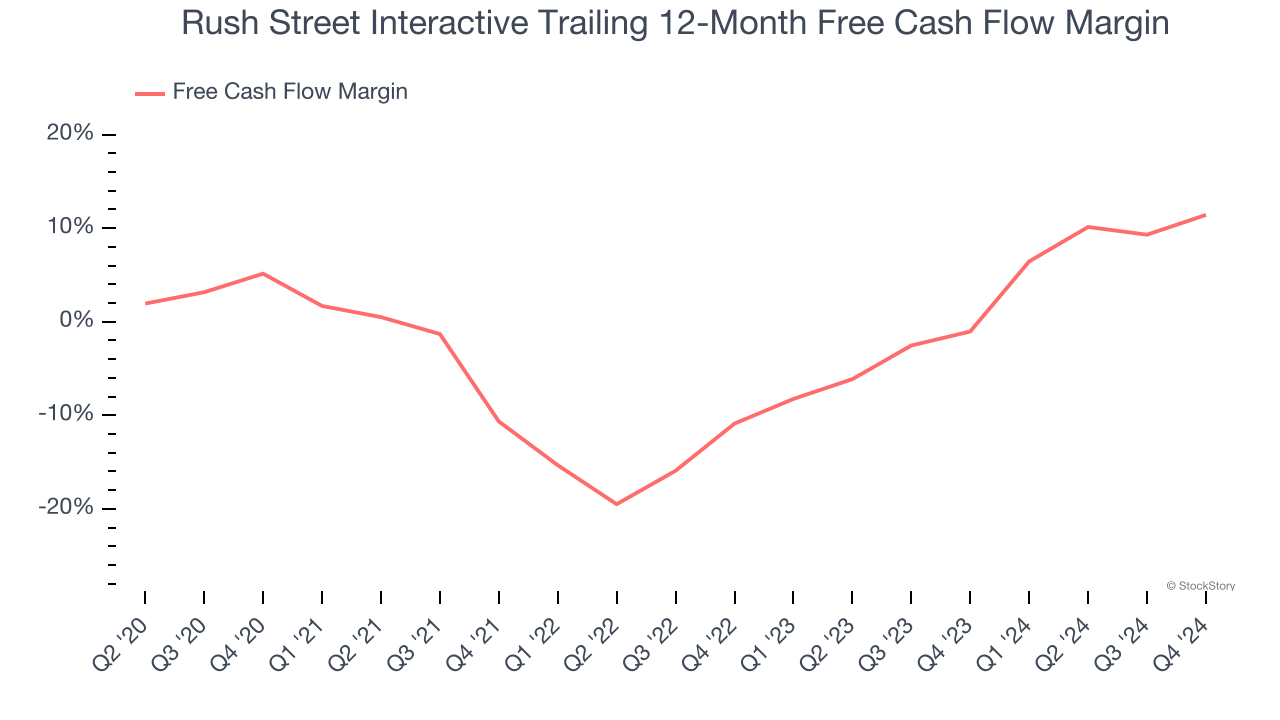

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Rush Street Interactive has shown weak cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 6.1%, subpar for a consumer discretionary business.

Final Judgment

Rush Street Interactive isn’t a terrible business, but it doesn’t pass our quality test. With its shares outperforming the market lately, the stock trades at 37.2× forward price-to-earnings (or $11.43 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - you can find better investment opportunities elsewhere. We’d suggest looking at one of our top digital advertising picks.

Stocks We Would Buy Instead of Rush Street Interactive

Market indices reached historic highs following Donald Trump’s presidential victory in November 2024, but the outlook for 2025 is clouded by new trade policies that could impact business confidence and growth.

While this has caused many investors to adopt a "fearful" wait-and-see approach, we’re leaning into our best ideas that can grow regardless of the political or macroeconomic climate. Take advantage of Mr. Market by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.